[전문요약]How does the LA production exodus accelerate?(탈 LA현상은 어떻게 가속화 되는가?)

미국 할리우드, 콘텐츠 인더스트리, 영화 분야 유명 팟캐스트인 “Strictly Business” 팟캐스트(Variety Intelligence Platform)의 최신 내용을 요약했다.

버라이어티의 새로운 연구 보고서 '프로덕션 파이프라인'이 나왔다. 이 팟캐스트는 보고서를 쓴 타일러 아퀼리나와 카레 에릭슨이 출연, 엔터테인먼트 산업의 중심부에서 벌어지고 있는 변화, 스트리밍 서비스의 향방, 제작 틀네드의 변화 등을 이야기한다.

1. 전체 개요

- 팟캐스트는 로스앤젤레스(이하 LA) 지역에서 발생한 대규모 산불이 영화 및 TV 제작 산업에 미치는 영향과, 이미 진행 중이던 ‘제작지 탈(脫)LA 현상(production exodus)’을 어떻게 가속화할 수 있는지에 대해 다룸.

- 또한 미국·영국의 제작비 증가, 세제 혜택 경쟁, 스트리밍 플랫폼들의 투자 축소, 박스오피스 동향, 프랜차이즈 의존도, 선댄스 영화제(Sundance Film Festival)에서의 작품 매매 동향 등이 다뤄짐.

- 궁극적으로 “LA가 과거처럼 제작 중심지 자리를 계속 유지할 수 있을까?”(Will LA remain the center of film/TV production?)라는 질문을 중심으로 논의.

The podcast examines the devastating impact of recent Los Angeles fires on film and TV production, the ongoing production exodus away from LA, and how these factors might accelerate one another. They also discuss the cost increases in the US and UK, tax credits, the reduction in streaming platform investments, box office trends, franchise dependency, and the latest Sundance Film Festival acquisition market. Ultimately, the conversation poses the question: “Will LA remain the center of production or not?”

2. LA 산불과 제작 산업에 대한 영향 (Los Angeles Fires & Impact on Production)

- 지난달 LA 지역을 휩쓴 대형 산불로 인해, LA에서 이미 감소세에 있던 영화·TV 제작이 추가 타격을 받을 가능성이 큼.

- 특히 현장 스태프(below-the-line workers)들이 주거와 재산 피해를 입어, 재정적으로 더 큰 고통을 겪을 우려가 있음.

- 다만 최근 제작 동향 자체가 LA에서 타 지역·해외로 분산되고 있어, 실제 제작 건수 측면에서의 즉각적 충격은 제한적일 수 있음.

Recent wildfires in Los Angeles have compounded the struggles of an already declining film and TV production sector in the region. Below-the-line workers face additional financial and personal hardships. Interestingly, because many productions have already migrated away from LA, the immediate overall production slowdown may be less dramatic than expected.

3. 제작지 탈(脫)LA 현상 (Production Exodus from LA)

- 지난 10여 년간 미국 내 다른 주(州)들과 해외가 세금 혜택(tax credits), 낮은 인건비 및 제작비를 앞세워 제작 유치를 적극 진행.

- 그 결과, LA의 미국 영화·TV 고용 비중은 2023년 약 27% 수준으로 하락(과거 약 32%→27%).

- 조지아, 루이지애나 등이 대표적 미국 내 대체 지역으로 떠오름(영국·동유럽 등도 대안지로 부상).

Over the past decade, many states and countries have lured productions with tax credits and lower labor/material costs. Consequently, LA’s share of US film/TV employment dropped to around 27% in 2023 (from 32% previously). States like Georgia and Louisiana, as well as Eastern European countries, have become major production hubs.

4. 캘리포니아 세액공제 확대 논의 (Tax Credit Expansion in California)

- 캘리포니아 주지사 Gavin Newsom은 현재 연간 3억3천만 달러 수준인 영화·TV 세액공제(캘리포니아 필름택스 크레딧)를 확대(7억5천만 달러)하려고 추진 중.

- 최근 산불 사태로 인해 이러한 세제 혜택 확대 또는 3년간 ‘무제한(unlimited) 택스 크레딧’을 요청하는 목소리가 업계에서 더욱 커짐.

- 그러나 이는 제한된 예산 문제 등으로 실현 가능성에 대한 논란이 있고, 설령 통과되더라도 과거와 같은 LA 제작 ‘독점 시대’를 되찾기 어려울 전망.

Governor Gavin Newsom seeks to raise California’s annual film/TV tax credits from $330 million to $750 million. In the wake of the fires, there’s industry pressure to uncap these credits for the next three years. However, budget constraints and broader economic factors suggest even an expansion won’t fully restore LA’s former production dominance.

5. 제작 허가(퍼밋) 비용 문제 (Permit Fees in LA)

- LA에서 촬영 퍼밋(permit)을 받는 비용이 매우 높아, 특히 저예산·독립영화 제작진에 큰 부담으로 작용.

- Film LA를 통해 퍼밋을 신청하는 데만 900달러 이상이 소요되며, 이는 최대 7일, 5개 로케이션까지만 유효.

- 업계는 “비싼 퍼밋 비용이 LA 제작 유입을 막는 원인 중 하나”라고 지적.

LA’s high permitting costs—over $900 just to apply for one permit—can significantly burden lower-budget productions. This fee only covers up to seven days of shooting and up to five locations, posing a major disincentive to film in the area.

6. 영국(UK) 제작 동향 (Production Trends in the UK)

- 영국도 제작비가 높은 편이어서 일부 제작사는 동유럽(체코, 헝가리 등)으로 이동 중.

- 영국 정부는 독립 제작사 유치를 위한 세제 개선을 시도하고 있음.

- 다만, 영국은 여전히 인기 촬영지이며, 세계적으로 성공한 드라마·영화에 안정적 기반 제공.

The UK also faces high production costs, prompting some filmmakers to relocate to Eastern Europe (e.g., the Czech Republic, Hungary). Although the UK government is revamping its tax incentives to attract independent producers, the region’s overall high costs still push many projects elsewhere. Nevertheless, it remains a major hub with a strong track record of globally successful titles.

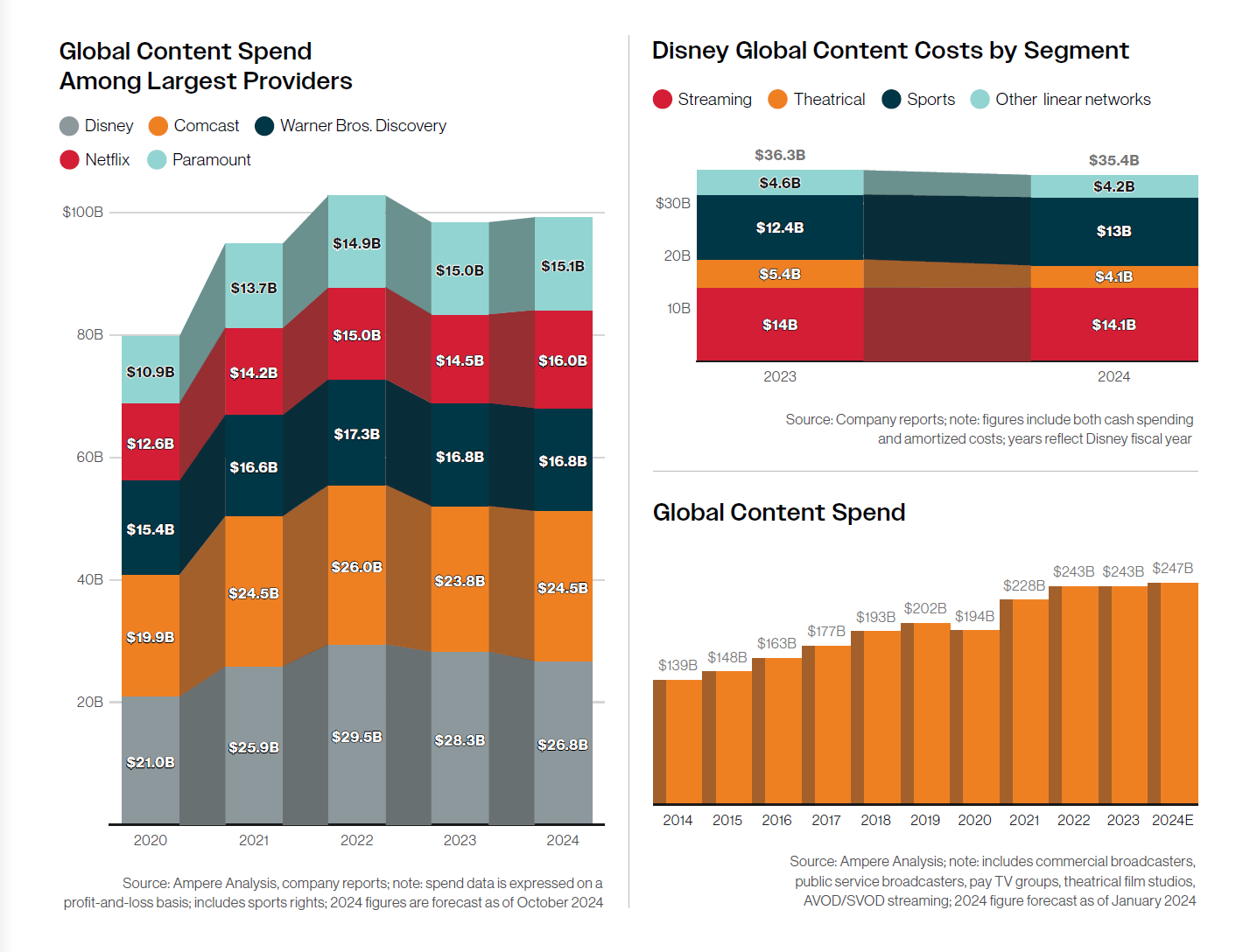

7. 스트리밍 투자 축소와 콘텐츠 지출 (Streaming Pullback & Content Spending)

- 글로벌 미디어 기업들이 콘텐츠 지출 확대에 신중해짐. 2025년 전체 콘텐츠 지출 증가율 전망은 전년 대비 +0.4%로 매우 제한적(출처: Ampere Analysis).

- 디즈니(Disney)는 2024년 240억 달러 예상 투자액을 230억 달러로 축소. 넷플릭스(Netflix)도 투자 증액을 최소화하며, 170~180억 달러 수준으로 유지할 전망.

- 이처럼 스트리밍 플랫폼의 지출 증가세 둔화로 인해 프로젝트당 예산이 더욱 제한되고, 제작지는 제작비 절감을 위해 저렴한 지역을 찾는 경향이 심화.

Media companies are reevaluating content spending: global content spend is expected to rise by just +0.4% in 2025 (Ampere Analysis). Disney cut its 2024 estimate from $24B to $23B, Netflix’s budget hovers around $17–18B. Tighter streaming budgets mean productions increasingly seek lower-cost locales.

8. 북미 박스오피스와 2025년 전망 (Box Office & 2025 Outlook)

- 2024년 박스오피스는 전년 대비 소폭 하락했으나, 예상보다 선방했다는 평가. 특히 애니메이션·공포 장르가 흥행 견인.

- 2025년 미국 내 와이드 릴리스(wide release) 영화는 약 110편으로, 2024년(95편)보다 증가할 전망(스트라이크 후 일정 재조정 효과).

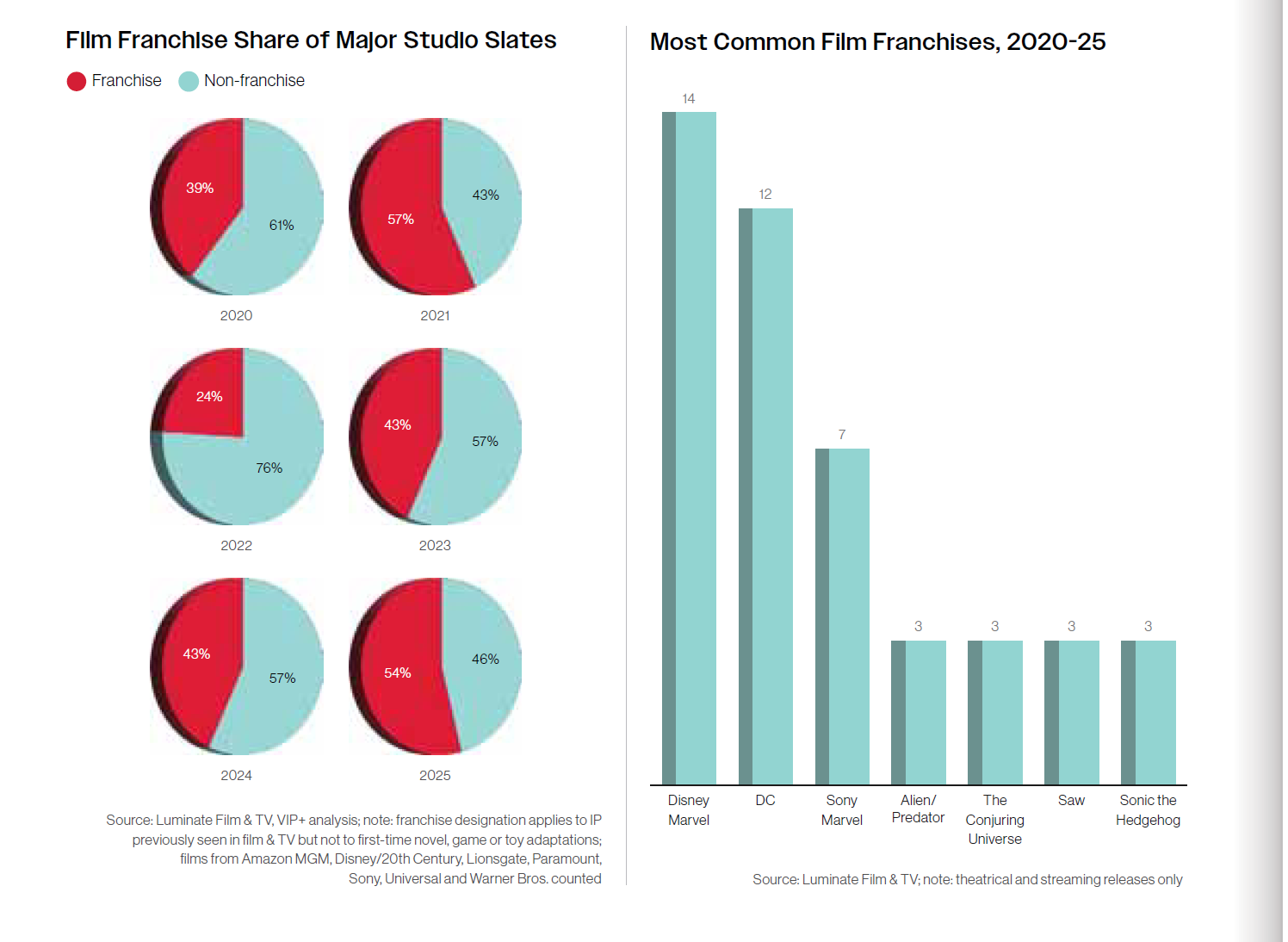

- 대규모 프랜차이즈에 의존하는 비율(약 54%)은 여전히 높으나, 일부 스튜디오가 완전히 새롭거나 예술(auteur) 작품에도 투자해 시장 다양화 시도.

The 2024 box office slightly dipped versus 2023 but surpassed many expectations, driven largely by animation and horror. In 2025, around 110 wide-release films are scheduled (up from 95 in 2024), partly due to post-strike rescheduling. Franchise dependency remains high at ~54%, though some studios are experimenting with new or auteur-driven projects to diversify.

9. 스트리밍 대비 극장 개봉 강화 (Shift from Streaming to Theatrical)

- 넷플릭스의 오리지널 영화 수는 여전히 많으나, 최근 대형 프로젝트(예: 그레타 거윅 감독의 <나니아 연대기> 각색)에 최소 4주간 극장 개봉을 허용하는 등, 극장 창구 활용이 늘어나는 추세.

- 디즈니, 아마존·MGM 등도 고예산 작품은 극장 개봉을 우선 검토. 결국 OTT 직행보다는 극장 선행 후 스트리밍 전략이 부상.

Netflix still produces a high volume of original films, but recent marquee deals (e.g., Greta Gerwig’s Narnia adaptation) include at least four weeks of theatrical exclusivity. Disney and Amazon/MGM also lean toward theatrical release for bigger-budget titles, signaling a shift away from straight-to-streaming models.

10. 프랜차이즈 의존도 (Franchise Dependency)

- 2025년 예고된 미국 주요 스튜디오 와이드 릴리스의 약 54%가 프랜차이즈에 속함.

- 소니(Sony)는 <28 Days Later>의 후속편·리부트 형태인 <28 Years Later>에 큰 예산을 투입해 새로운 장기 시리즈화를 모색.

- 전체적으로는 2019년 전후 “프랜차이즈 범람” 수준까지는 아직 아니지만, 여전히 IP 기반 시리즈가 흥행 안전판으로 작동.

Around 54% of 2025 wide releases from major studios are tied to existing franchises. Sony is heavily investing in a new trilogy based on “28 Days Later” (titled “28 Years Later”). While not at the peak saturation of 2019, IP-based projects remain a key revenue and audience driver.

11. 선댄스 영화제(Sundance Film Festival) 동향

- 올해 선댄스는 예년과 비슷한 규모(80~100편)로 진행되었으나, 매수·판매는 초반에 다소 ‘조용’ 했다가 후반부에 어느 정도 회복.

- 주요 OTT들의 적극적 구매가 예전만 못하다는 평가. 예) 넷플릭스의 대규모 딜이 크게 줄어든 상황.

- 공포·장르 영화에 대한 미니배급사(예: 네온, A24) 등의 관심 증가.

Sundance maintained its usual volume of 80–100 titles, but acquisitions were slower early on, then picked up slightly. Streamers, notably Netflix, were less aggressive in major deals. Distributors like Neon showed continued interest in genre/horror films, which remain strong box office performers.

12. 시상식(오스카 등) 전망 (Oscars & Awards)

- 2024~2025시즌, A24 등 예술성 높은 작품이 박스오피스에서도 선전하며 주목받음.

- 글로벌 시상식에서 수상 가능성이 높은 작품들이, 극장 관객 동원에도 긍정적 영향을 미치는 경향이 재확인됨(“상업성과 비평적 성취의 공존”).

Films like A24’s The Brutalist are garnering both box office attention and award-season buzz. The interplay between commercial success and critical acclaim remains evident, indicating that well-crafted, award-caliber films can still resonate in theaters.

마무리 (Conclusion)

- LA 지역 제작 산업은 산불 및 기존 비용 부담, 그리고 타 지역의 세제 혜택 경쟁에 맞서 어려운 상황을 겪고 있음.

- 그러나 LA의 기반 시설, 인재풀, 오랜 역사적 노하우가 여전히 강력하기에, 제도적 보완(세액공제 확장, 퍼밋 비용 재검토)과 업계 내 유대가 강화되면 ‘제작 중심지’ 지위를 유지할 가능성도 남아 있음.

- 장기적으로는 국내외 다양한 제작 허브들이 공존하며, 스트리밍 vs. 극장, 프랜차이즈 vs. 오리지널 사이의 균형점을 찾는 추세가 이어질 것으로 전망.

LA’s film/TV sector is under strain due to wildfires, high costs, and competition from other regions offering generous incentives. Still, LA retains robust infrastructure, talent pools, and industry expertise. With policy adjustments (e.g., expanded tax credits, lower permit fees) and strengthened industry collaboration, LA could maintain its production hub status. Long term, a multi-hub global model seems likely, balancing streaming vs. theatrical releases and franchise vs. original content.

![[Report]Inclusion & Equity Report 2025 by WGA](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/05/dza9ol_202505310259.png)

![[Report]라이선싱엑스포 2025 심층 보고서](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/05/srjw47_202505191926.png)