Overview of the “2024 Korea Broadcasting Market Competition Assessment”

1. Background & Purpose

Conducted By: The Korea Communications Commission (Chairperson: Lee Jin-sook) in cooperation with the Korea Information Society Development Institute (KISDI).

Scope of Data:

2023 data sources: Broadcasting industry fact-finding surveys, financial reports, and broadcast business financial disclosures.

2024 surveys: Additional feedback from users (viewers), production companies, and advertisers.

Markets Evaluated:

Pay TV (subscription) market

Broadcast channel transaction market

Broadcast video content transaction market

Broadcast advertising market

2. Key Findings by Market Segment

I. Pay TV Market

A. Market Definition & Current Status

The Pay TV market includes Internet Protocol TV (IPTV), Cable TV (SO), and Satellite TV operators that offer subscription-based services.

Subscribers & Revenues

As of 2023, total Pay TV subscribers reached 36.29 million (household connections), a negligible increase of 0.01% from the previous year.

Pay TV revenue (from broadcast-related activities) stood at 7.2328 trillion KRW, a 0.4% increase year-over-year, indicating a slowing growth trend.

Shift Toward IPTV & Competition from OTT

IPTV accounted for 57.8% of all Pay TV subscribers in 2023, up from the previous year (57.0% in 2022). Cable TV share fell to 34.3% (previously 35.0%).

The market’s stagnation is largely attributed to high saturation and increased competitive pressure from online video services (OTT).

Concentration & ARPU

The top 3 IPTV operators (KT, LG Uplus, SK Broadband) collectively make up 86.8% of Pay TV subscribers and 91.4% of Pay TV revenue—further strengthening what is effectively an oligopoly.

Average revenue per user (ARPU) has been decreasing, especially for VOD services, due to heightened OTT competition.

Despite this oligopolistic structure, no significant evidence of negative price impacts on consumer welfare (e.g., ARPU has actually declined).

B. Implications

Growth Slowdown

Saturation of the subscriber base, shifting consumer viewing habits, and intense OTT competition all weaken the Pay TV growth potential.

IPTV still shows incremental growth, but the pace is slowing. Cable TV is consistently losing subscribers.

Oligopoly & Potential Effects

The three major IPTV operators continue to dominate. However, their pricing power with end consumers is not clearly manifesting as higher ARPU; instead, ARPU has decreased.

The main area where their market power appears to have impact is in channel and home-shopping transaction fees.

Future Disruptions

Emerging services like FAST (Free Ad-Supported Streaming TV), while still nascent in Korea, are growing in some overseas markets, potentially altering the competitive landscape and substituting or complementing existing pay TV or OTT models.

II. Broadcast Channel Transaction Market

A. Market Definition & Current Status

This market involves wholesale transactions between:

Pay TV operators (IPTV, Cable, Satellite) as buyers, and

Terrestrial (broadcast) networks and Program Providers (PPs) as sellers (the “broadcast channel transaction market”).

Revenue

Total channel carriage fees (retransmission fees) paid to terrestrial broadcasters and PPs reached 1.494 trillion KRW in 2023, up 9.3% from 1.3674 trillion KRW in 2022.

The increase is driven by a 8.4% rise in PP fees and an 11.3% increase in terrestrial retransmission fees.

Viewership Trends

Overall TV viewing time has declined since 2020, including both terrestrial and pay TV channels.

Daily average TV viewing in 2023 was 121 minutes, down 24.8% over the last three years. The shift is attributed to the growing use of OTT platforms rather than viewers moving from pay TV channels to terrestrial channels.

B. Market Concentration & Negotiation Dynamics

Concentration Ratios

The top provider (CJ Group) holds an 18.7% share (by channel sales revenue). The market’s Herfindahl-Hirschman Index (HHI) stands at 983, which is below the threshold typically concerning for competition regulators.

This suggests that competition-restraining practices from the supply side (channel providers) are unlikely.

Negotiation Power

Demand Side (Pay TV Operators): Highly concentrated (HHI 2,624), suggesting strong bargaining leverage when negotiating channel carriage fees.

Supply Side (Channel Providers): Popular channels (particularly top terrestrial channels and highly rated PP channels) have countervailing power. If these channels are dropped, pay TV operators risk losing subscribers.

C. Implications

While overall market concentration on the supply side is low, the “must-carry” nature of premium channels could increase the risk of disputes.

Ongoing monitoring is essential due to changing incentives (e.g., declining broadcast advertising revenues may push channel providers to seek higher retransmission fees).

Increased competition from OTT may either strengthen or weaken channel providers’ negotiating position.

III. Broadcast Video Content Transaction Market

A. Market Definition & Current Status

This market covers transactions for broadcast video content (TV programs, drama, etc.) between:

Buyers: Terrestrial broadcasters, PP channels, and OTT platforms

Suppliers: Production studios (external or affiliated)

Shift in Market Boundaries

The old definition of “broadcast program transaction” is broadened to account for OTT original content, reflecting how OTT operators compete with traditional broadcasters for quality productions.

Domestic Production Trends

Total direct production spending by broadcasters (including in-house, outsourced, and licensed programs) was 2.9034 trillion KRW in 2023, up 0.9% from 2.8774 trillion KRW in 2022.

However, outsourcing production hours actually dropped 15.8%, suggesting lower overall demand for domestic broadcast content.

OTT Dynamics

Major global OTTs, particularly Netflix, have increased their investment in Korean content.

Domestic OTT platforms, however, face financial pressures from shrinking ad markets and rising production costs, leading to fewer original productions.

B. Market Concentration & Global OTT Influence

The HHI for overall broadcast production spending among broadcasters is 906, which remains relatively low—no strong sign of dominant behavior by a single broadcaster or group.

However, the growing dependence on Netflix and other global OTTs raises concerns about the “buyer power” these platforms could wield if local broadcasters and OTTs scale back their content investments.

C. Implications

Reduced Domestic Demand

The previously fast-growing demand for Korean content (driven by global OTT interest) cooled in 2023, notably because domestic OTT operators and broadcasters face budget constraints.

Netflix’s Role

Netflix’s rising investments in Korean content could reshape power dynamics in content negotiations, potentially over-concentrating influence in the hands of a few global players.

Data Gaps

Lack of comprehensive OTT data—particularly around production costs and investments in originals—hampers full market analysis. Regulatory and statistical improvements are needed.

IV. Broadcast Advertising Market

A. Market Definition & Current Status

The “broadcast advertising” market includes real-time TV commercials sold by:

Terrestrial broadcasters

Cable channels

Pay TV operators

Overall Advertising Landscape

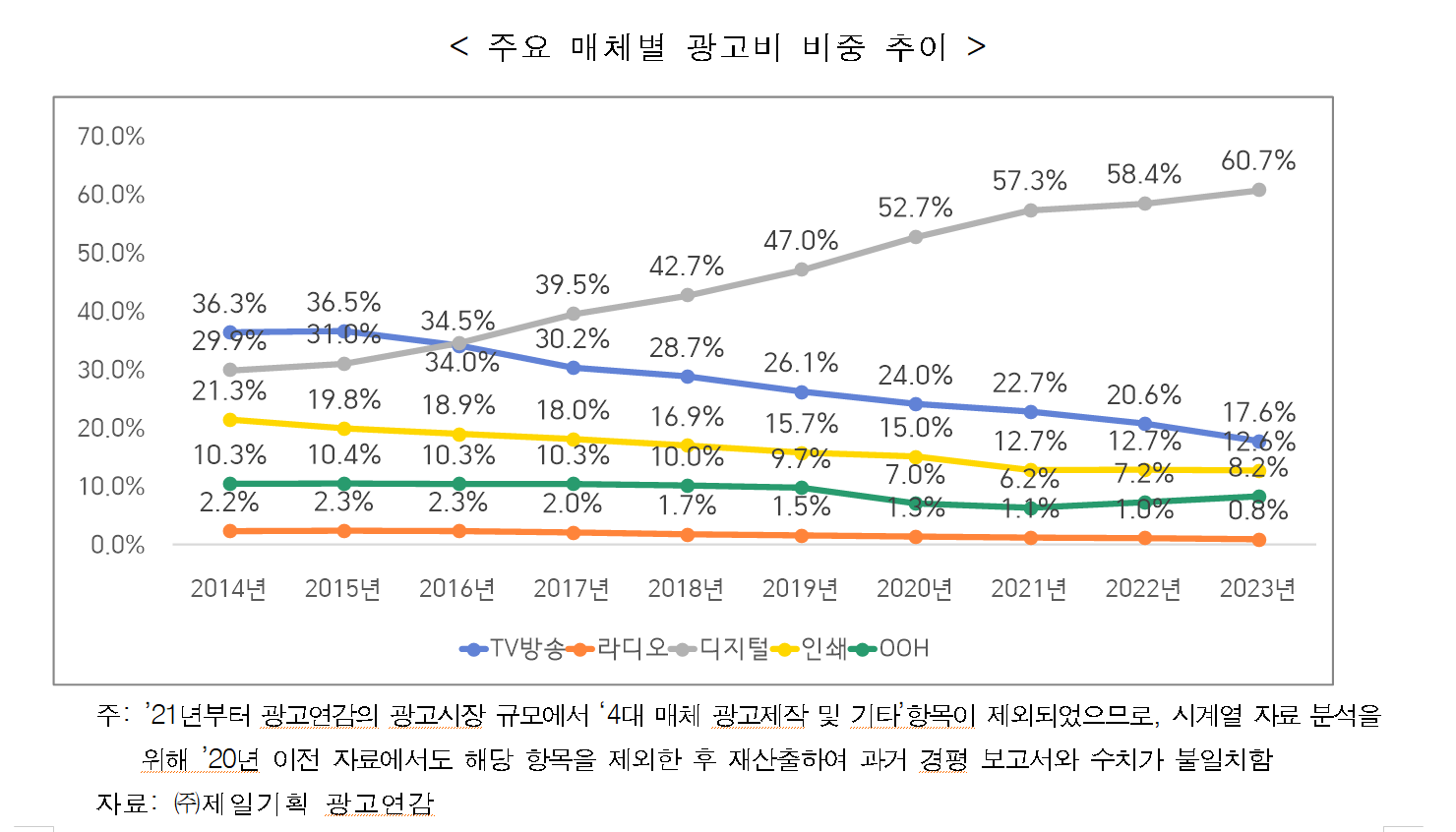

Korea’s total ad market in 2023 reached 13.8017 trillion KRW, down 0.6% from 2022.

Broadcast advertising revenue fell 18.5% year-over-year to 2.3574 trillion KRW, marking a significant decline.

Broadcast’s share of the overall ad market dropped to 17.6%, continuing its downtrend (22.7% in 2021 → 20.6% in 2022 → 17.6% in 2023).

Digital advertising now accounts for 60.7% of the total ad market, up 2.3 percentage points from the previous year.

Shifting Advertiser Perceptions

Traditionally, advertisers valued linear TV for broad reach and impact.

Recent surveys show a narrowing gap between broadcast TV ads and OTT ads in perceived effectiveness and cost-efficiency.

B. Market Concentration

The HHI for broadcast advertising revenue was 935 in 2023, down from 1,028 in 2022, indicating no significant concentration concerns at the aggregate level.

C. Implications

Declining Competitiveness of Linear TV

Digital and OTT platforms are steadily overtaking traditional broadcast in the advertising sector.

Expanded Competitive Boundaries

Broadcast advertising no longer competes solely within its own domain; it’s part of a broader landscape including digital and OTT platforms.

Assessments of the broadcast ad market thus require a more holistic approach that considers cross-media competition, audience migration to digital platforms, and innovations in ad tech.

Overall Conclusions & Future Outlook

Evolving Market Definitions

The 2024 assessment consolidates previously separate markets (e.g., combining cable vs. terrestrial channels) to reflect how OTT and shifting viewer behavior affect all players.

Regulatory practices are adapting to a reality where traditional broadcast and OTT services overlap and compete in content acquisition, channel carriage, and advertising.

Strengthening Oligopoly in Pay TV

The top three IPTV operators continue to dominate the subscription market. However, they face external competition from OTT platforms, limiting their pricing power over end consumers.

Decreasing Demand for Domestic Broadcast Content

While global OTT (especially Netflix) invests heavily in Korean content, domestic broadcasters and OTTs show reduced demand (due to falling ad revenue and financial pressures).

This dynamic could grant more negotiating leverage to global streaming platforms.

Broadcast Advertising’s Ongoing Decline

Broadcast advertising continues to shrink relative to the broader ad market, mostly supplanted by digital and OTT ads. Advertisers increasingly view OTT ads as similarly effective—if not more so.

Implications for Policy & Regulation

Monitoring & Data Gaps: The need for robust data—including OTT spending—remains critical to fully grasp market dynamics and make informed policy decisions.

Competition Enforcement: Regulators must watch for potential abuses of bargaining power—whether it’s Pay TV operators in channel negotiations or global OTTs in content acquisitions.

Public Interest & Innovation: As the broadcast sector’s influence wanes in the ad market, policy makers must balance the public-interest goals historically tied to broadcast media with the realities of a market increasingly dominated by digital platforms.

Overall, the 2024 assessment underscores a rapidly transitioning Korean media environment where linear TV markets remain sizable but face stagnation and intensifying competition from OTT. The KCC plans to publish a comprehensive report, along with supporting data and graphics, on both its official website (www.kcc.go.kr) and the Broadcast Statistics Portal (mediastat.or.kr).

![[보도자료]Kocowa, 유럽 진출 1년 성과](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/07/d4i5qa_202507142153.png)