Why Telecom Companies Are Failing in the Streaming Wars (통신사는 스트리밍 전쟁에서 왜 매번 실패하는가?)

‘이제는 스트리밍이 아닌 스트리밍 통합 플랫폼(aggregator) 전쟁이다.’

그러나 이 시장에서 통신사는 왜 실패하는가? 버라이즌의 백기 투항

- 버라이즌 ‘스트리밍 통합 플랫폼 ‘+play’ 철수 선언, SVOD의 비협조

- 대신 차터의 ‘케이블TV와 스트리밍 묶음 번들’의 절반성공

- 승자는 ‘유통 대기업’.

- 아마존 프라임 비디오, 애플TV플러스도 품은 아마존 프라임 채널스

- 비지오 인수한 월마트도 스트리밍 플랫폼 시장 진입

The Battle Has Shifted from Individual Streaming Services to Streaming Aggregation Platforms

Verizon withdraws its streaming aggregation platform '+play' amid SVOD resistance

Charter's cable TV-streaming bundle strategy shows moderate success

Winners emerge as 'retail giants': Amazon Prime Video Channels dominates while Walmart enters through Vizio acquisition

2025년, 스트리밍 산업의 주도권을 둘러싼 경쟁이 새로운 국면에 접어들고 있다. 불과 몇 년 전만 해도 각종 구독형 동영상 서비스(SVOD)들이 저마다 독립적으로 시장을 확장하며 '스트리밍 전쟁'을 벌였다면, 이제는 수많은 구독 스트리밍 서비스를 하나로 묶어주는 '통합 플랫폼(aggregator)'이 대세다. 스트리밍 통합 플랫폼은 더 많은 구독자를 끌어모으고 스트리밍 서비스들에게도 수수료를 받을 수 있어 '비즈니스의 지속 가능성'을 높인다.

최근 통신사 버라이즌(Verizon)이 자체 SVOD 통합 플랫폼 '+play'의 운영을 종료하면서 통신사의 퇴장이 현실화된 반면, 케이블TV 1위 차터 커뮤니케이션즈(Charter Communications)는 디즈니+(Disney+), 훌루(Hulu), 맥스(Max), 피콕(Peacock), 파라마운트+(Paramount+) 등 대형 SVOD를 케이블 패키지에 포함시키며 기존 유료방송 가입자 이탈을 크게 줄이고 있다.

이와 동시에 아마존(Amazon)은 프라임 비디오 채널즈(Prime Video Channels)를 통해 미국 SVOD 신규 가입의 4분의 1을 차지하며 통합 플랫폼 시장의 절대 강자로 부상했다. 한편 월마트(Walmart)는 비지오(Vizio) 인수를 통해 스마트 TV와 자체 운영체제를 결합한 새로운 스트리밍 통합 플랫폼을 구축, 본격적으로 시장에 뛰어들었다. 소비자들은 더 이상 여러 개의 SVOD를 개별 구독하는 '스태킹'에 피로감을 느끼고, 업계는 다시 '통합' 모델로 회귀하는 흐름이 뚜렷해지고 있다.

이처럼 버라이즌의 퇴장, 케이블의 반격, 아마존의 독주, 그리고 월마트의 신흥 도전이 얽히며, 2025년 스트리밍 통합 플랫폼 전쟁은 그 어느 때보다 치열하고 복잡한 양상으로 전개되고 있다. 누가 스트리밍 구독의 '관문'을 장악할 것인가—이 질문이 미디어 산업의 미래를 좌우하는 최대의 화두로 부상했다.

특히 통신사들의 연이은 실패는 KT, SK텔레콤, LG유플러스 등 국내 통신 3사에게도 시사하는 바가 크다. 막대한 기술 인프라와 수천만 고객 기반을 보유했음에도 버라이즌이 스트리밍 통합에서 실패한 것은, 단순한 기술력과 가입자 수만으로는 이 새로운 전장에서 승리할 수 없음을 보여준다. 대신 유통 노하우와 생태계 구축 능력을 가진 아마존과 월마트 같은 기업들이 주도권을 잡아가고 있다. 이는 국내에서도 쿠팡, 이마트, 롯데마트 등 유통 플랫폼들이 스트리밍 통합 서비스에서 새로운 기회를 모색해야 함을 시사한다.

누가 스트리밍 구독의 '관문'을 장악할 것인가—이 질문이 미디어 산업의 미래를 좌우하는 최대의 화두로 부상했다.

In 2025, the competition for control of the streaming industry has entered a new phase. While subscription video-on-demand (SVOD) services once competed independently to expand their market reach in the so-called "streaming wars," the focus has now shifted to streaming "aggregation platforms" that bundle multiple subscription services together. These aggregation platforms can attract more subscribers while collecting fees from streaming services, enhancing business sustainability.

The recent shutdown of Verizon's SVOD aggregation platform '+play' marks the telecom industry's retreat from this space, while Charter Communications, the nation's largest cable TV operator, has significantly reduced subscriber churn by bundling major SVOD services like Disney+, Hulu, Max, Peacock, and Paramount+ into their cable packages.

Meanwhile, Amazon has emerged as the dominant force in the aggregation platform market through Prime Video Channels, capturing approximately 25% of new SVOD subscriptions in the United States. Walmart has also entered the fray by acquiring Vizio, combining smart TV hardware with its own operating system to build a new streaming aggregation platform. As consumers grow weary of "stacking" multiple individual SVOD subscriptions, the industry is clearly returning to an "aggregation" model.

The interplay of Verizon's withdrawal, cable TV's counterattack, Amazon's dominance, and Walmart's emerging challenge has made the 2025 streaming aggregation platform war more intense and complex than ever. The question of who will control the "gateway" to streaming subscriptions has become the defining issue for the future of the media industry.

The repeated failures of telecom companies hold significant implications for domestic players like KT, SK Telecom, and LG Uplus. Despite Verizon's massive technical infrastructure and tens of millions of customers, its failure in streaming aggregation demonstrates that technical capability and subscriber numbers alone cannot guarantee victory in this new battlefield. Instead, companies with retail expertise and ecosystem-building capabilities like Amazon and Walmart are seizing control. This suggests that domestic retail platforms like Coupang, E-Mart, and Lotte Mart should explore new opportunities in streaming aggregation services.

통신사들의 엇갈린 운명: 버라이즌의 철수와 차터의 부상

스트리밍 통합 시장에서 통신사들의 운명이 극명하게 갈리고 있다. 버라이즌의 +플레이 서비스 종료(7월 9일)는 단순한 사업 철수를 넘어서 통신업계가 스트리밍 생태계에서 주도적 위치를 차지하는 것이 얼마나 어려운 일인지를 보여주는 상징적 사건이다.

대신 버라이즌은 ‘myPlan’과 ‘myHome’ 패키지로 스트리밍 번들 제공을 이어간다는 전략이다. 버라이즌은 성명서를 통해 마이플랜(myPlan)과 마이홈(myHome) 패키지가 +플레이의 "진화된 형태"라고 설명했지만, 이는 본질적으로 독립적인 구독 마켓플레이스 운영에서 단순한 번들 서비스 제공으로의 후퇴를 의미한다.

이에 대해 버라이어티 타일러 아퀴리나(Tyler Aquilina)기자는 “버라이즌의 +플레이 서비스는, 통신사들이 언젠가는 꼭 뛰어들어야 할 스트리밍 통합(여러 스트리밍 서비스를 한데 모아주는) 분야에서 먼저 시작한 만큼 의미가 컸다”며 “하지만 +플레이가 실패했다는 사실은, 앞으로도 당분간은 통신사들이 이 시장에서 중심 역할을 하기는 어렵다는 걸 보여준다”고 말했다.

스트리밍 서비스 시장에서 통신사의 패배는 두 가지로 요약된다. 방송 콘텐츠 시장에 대한 이해와 전략 부족과 아마존이나 월마트와 같은 유통 대기업에 비해 턱없이 떨어지는 '오디언스 집합력(Aggregator).

결국 통신사들은 콘텐츠 시장도 장악하지 못하고 구독자들의 마음을 얻는데도 실패하고 있다. 이제 커뮤니케이션의 주도권도 통신사가 아닌 소셜 미디어나 틱톡이 보유하고 있다.

반면 케이블TV는 다르다. 규모가 크진 않아도 방송은 잘 안다.

반면 케이블TV 사업자 차터 커뮤니케이션즈는 완전히 다른 길을 걷고 있다. 이 회사는 놀라울 정도로 빠른 속도로 광고 지원 구독 스트리밍 서비스(SVOD)들의 라인업을 구축했으며, 이를 고객들에게 추가 비용 없이 제공하고 있다. 더 나아가 고객들은 차터(Chater)를 통해 이들 스트리밍 서비스들의 광고 없는 버전도 구매할 수 있으며, 차터는 이로부터 구독 수익의 일정 부분을 가져가는 것으로 추정된다.

The Divergent Fates of Telecom Companies: Verizon's Retreat vs. Charter's Rise

The fortunes of telecom companies in the streaming aggregation market are starkly divided. Verizon's termination of its +play service (July 9) represents more than just a business withdrawal—it's a symbolic event demonstrating how difficult it is for telecom companies to achieve a leading position in the streaming ecosystem. Instead, Verizon continues its streaming bundle offerings through 'myPlan' and 'myHome' packages. While Verizon described these packages as an "evolved form" of +play, this essentially represents a retreat from operating an independent subscription marketplace to providing simple bundle services.

Variety reporter Tyler Aquilina commented: "Verizon's +play service was significant because it was an early entry into streaming aggregation—a field that telecom companies would eventually need to enter. However, the failure of +play shows that telecom companies will likely struggle to play a central role in this market for the foreseeable future."

In contrast, cable TV operator Charter Communications has taken a completely different path. The company has built an impressive lineup of ad-supported subscription streaming services at remarkable speed, offering them to customers at no additional cost. Furthermore, customers can purchase ad-free versions of these streaming services through Charter, with the company presumably taking a percentage of subscription revenue.

미국 주요 SVOD 번들 현황

출처(Source): Variety Intelligence Platform analysis

※ 일부 번들은 한시적 프로모션이나 특정 조건에만 해당될 수 있다.

차터의 이러한 전략의 성공은 수치로도 확인된다. 2025년 1분기 차터는 18만1,000명의 케이블TV(비디오) 고객을 잃었는데, 이는 분명히 승리라고 할 수는 없지만 2024년 1분기 40만 5,000명 손실에 비하면 엄청난 개선이다. 이는 차터 구독 패키지에 주요 스트리밍 서비스들이 추가된 것이 주요 요인으로 보인다. 즉, 차터 케이블TV를 구독하면 유료 스트리밍 서비스를 무료로 볼 수 있다는 장점이 ‘케이블TV’ 구독자를 유지시켰다는 이야기다.

Charter Video Subscriber Growth YoY(차터 비디오 가입자 연간 성장률)

출처(Source): company reports, MoffettNathanson

차터는 2023년 가을 디즈니와 SVOD번들링 계약을 처음 진행했다. 그러나, 처음엔 차터와 디즈니 간 프로그램 사용료 갈등 때문이었지만, 시간이 지나면서 라인업은 더욱 강화되었다. 2024년 8월 파라마운트+가 추가되었고, 올해(2025년) 초에는 피콕(Peacock)이 합류했다. 모펫네이선슨(MoffettNathanson)의 애널리스트들은 차터의 1분기 실적 발표 후 밝힌 4월 리서치 노트에서 "차터의 번들 스트리밍 패키지의 초기 효과를 보기 시작하는 것으로 보인다"고 분석했다.

이런 ‘케이블TV와 스트리밍’ 번들 전략이 케이블TV의 궁극적인 운명을 구원할 가능성은 여전히 낮다. 하지만, 차터의 제한적 성공은 유료 방송 시장 다양한 번들링과 상품 출시 경험이 많은 ‘유료 방송 사업자’들이 스트리밍 시대에도 시장 방어 능력이 있다는 것을 의미한다.

Charter's success with this strategy is evident in the numbers. In Q1 2025, Charter lost 181,000 cable TV (video) customers—while certainly not a victory, this represents a dramatic improvement from the 405,000 losses in Q1 2024. This improvement appears largely attributable to the addition of major streaming services to Charter's subscription packages. In essence, the ability to access premium streaming services for free with a Charter cable TV subscription has helped retain cable TV subscribers.

하지만 미래는 밝지 않다. 케이블 TV나 위성방송의 자금력과 가입자로는 아마존(Amazon)이라는 "모든 것을 파는 상점"과는 경쟁하기 어려울 것으로 보인다. 아마존의 프라임 비디오 채널즈(Prime Video Channels) 서비스는 지배적인 ‘스트리밍 통합 플랫폼이 되는 것은 시간 문제다. 아마존 프라임 비디오 채널즈는 아마존 프라임(Prime) 또는 프라임 비디오(Prime Video) 회원이 별도의 월정액을 추가로 지불하고 HBO Max, Paramount+, Starz, Showtime 등 다양한 프리미엄 스트리밍 서비스를 자신의 프라임 비디오 계정에 추가해 한 곳에서 관리·시청할 수 있는 서비스다. 한국 유일의 글로벌 스트리밍 서비스 코코와(Kocowa)도 아마존 채널스에서 구독할수 있다.

아마존의 압도적 우위와 그 의미

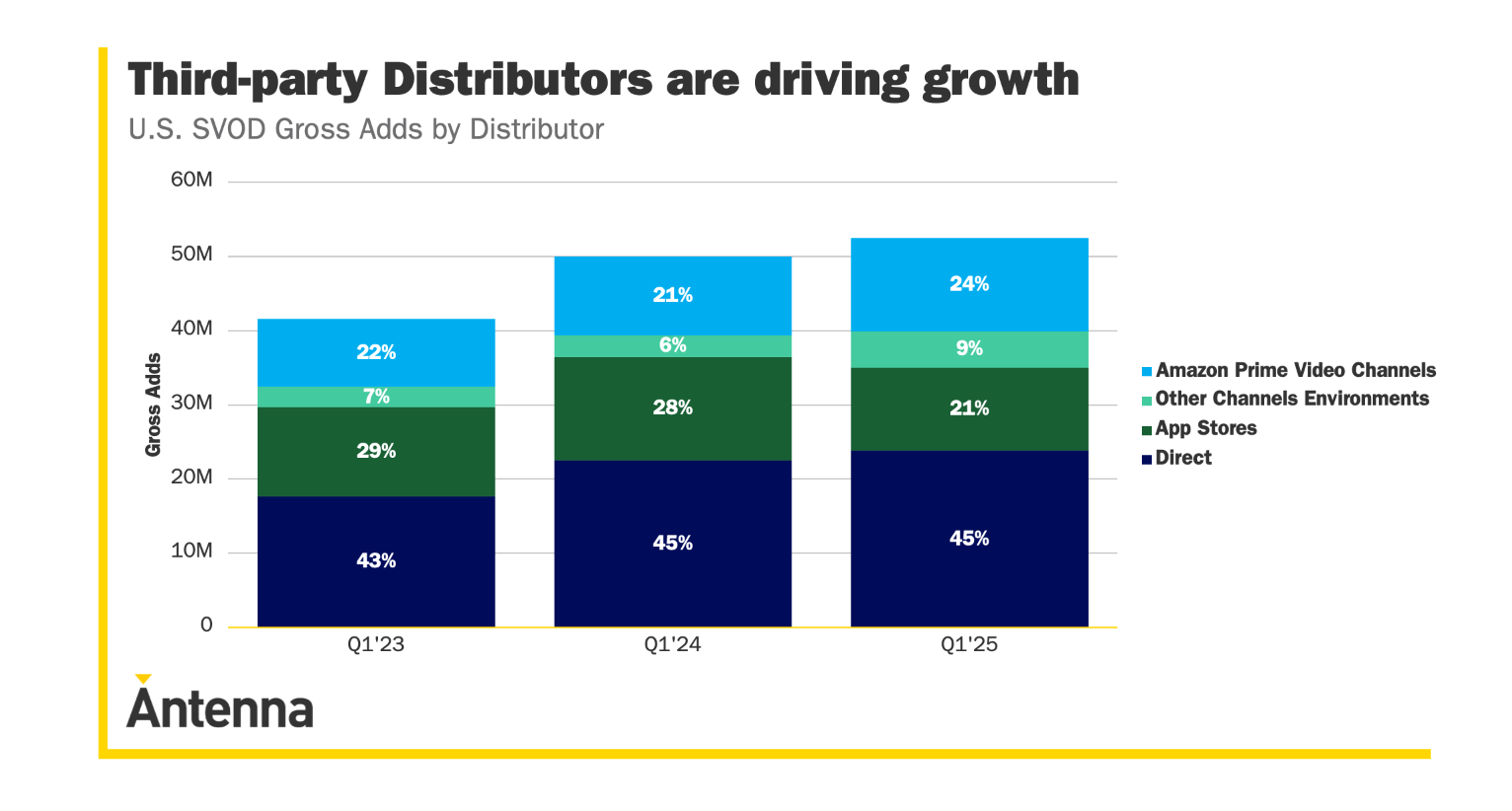

최근 업계 행사에서 아마존은 자신들이 의뢰한 안테나(Antenna)의 연구 보고서를 공개했다. 이 보고서에 따르면 프라임 비디오 채널즈를 통한 구독이 2025년 1분기 미국 SVOD 가입의 약 25%를 차지했다. 안테나의 데이터에 따르면, 이는 e-커머스 거대 기업인 아마존을 제3자 유통업체 중 압도적인 1위로 올려놓았으며, 애플(Apple)과 구글 플레이(Google Play)를 포함한 모든 주요 앱스토어를 합친 것보다 더 큰 점유율이다.

이전 안테나 보고서들은 아마존의 우위가 주로 프리미엄 플랫폼보다는 소규모 "전문" SVOD 구독 서비스에서 나온다고 지적했다. 즉 다른 곳에서 제공하지 않는 전문 스트리밍 서비스를 공급하기 때문에 아마존을 통해 구독을 한다는 이야기다. 그러나 이제는 상황이 바뀌었다. 그럼에도 불구하고 아직은 대형 스트리밍 서비스들은 아마존과 거래하지 않는다. 넷플릭스(Netflix), 디즈니+, 피콕까지도 여전히 프라임 비디오 채널즈에 참여하지 않고 있다. 하지만, 상황은 바뀌고 있다. 애플 TV+(Apple TV+)가 채널즈 라인업에 추가된 것은 통합 분야에서 아마존이 주요 빅테크 경쟁사보다 우위에 있음을 보여주었다.

미국 SVOD 신규 가입자(총합) 유통채널별 비중 변화(U.S. SVOD Gross Adds by Distributor)

- 직접(Direct): 스트리밍 서비스 공식 웹사이트 또는 앱에서 직접 가입

- 앱스토어(App Stores): 애플 앱스토어, 구글 플레이스토어 등 모바일 앱마켓을 통한 가입

- 기타 채널(Other Channels Environments): 통신사, 케이블, 번들 등 기타 유통채널

- 아마존 프라임 비디오 채널즈(Amazon Prime Video Channels): 아마존의 프라임 비디오 내 채널 구독 기능을 통한 가입

출처: Antenna, 2025년 1분기 기준

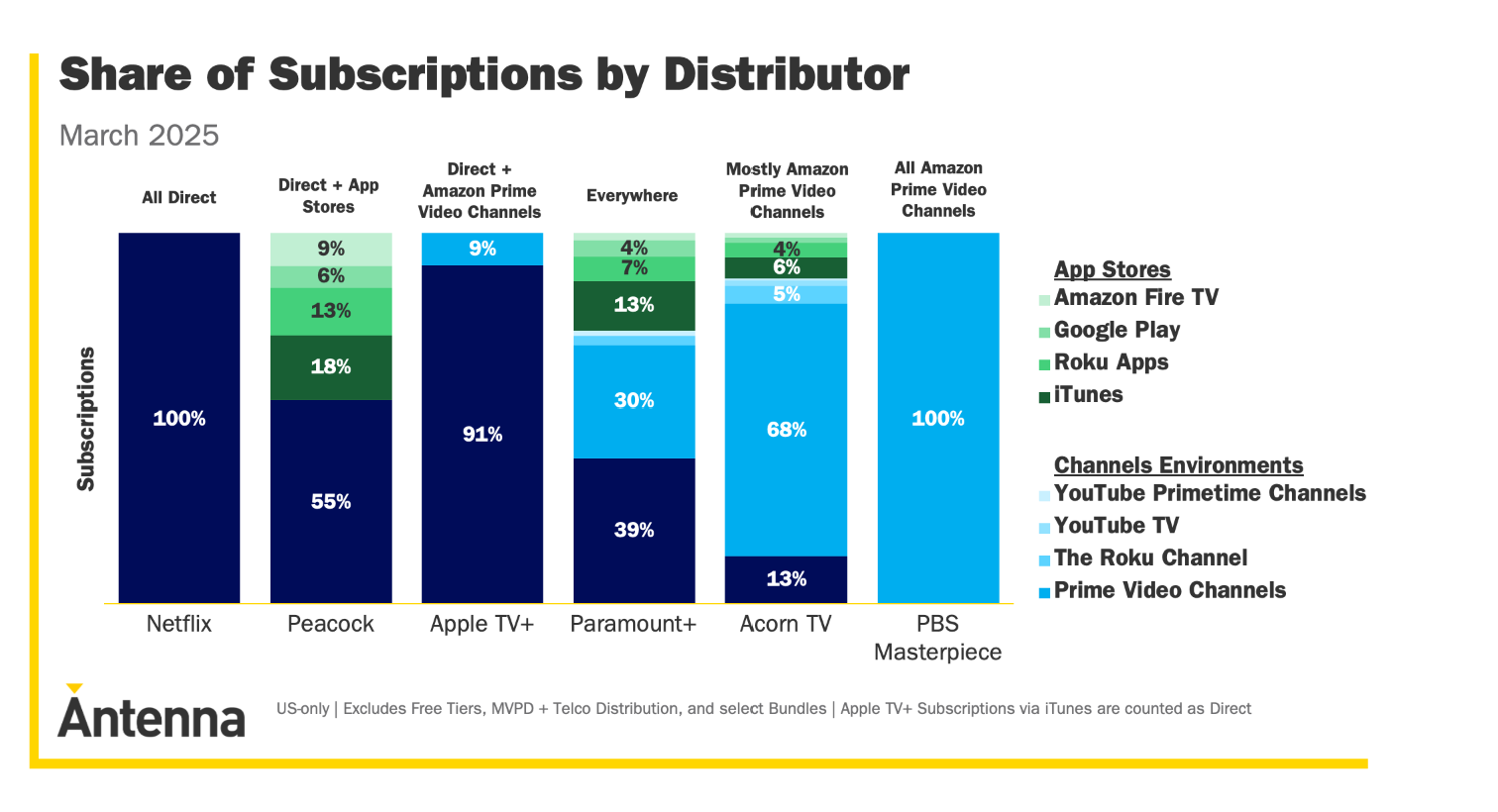

애플TV플러스의 경우 프라임 비디오 채널즈에 합류가 긍정적인 효과를 냈다. 프라임 비디오 합류 이후 가입자가 급증했다. 보고서는 또 HBO 맥스(HBO Max)가 2021년 프라임 비디오와의 유통 계약을 종료한 후 약 500만 구독자를 잃었다가, 이듬해 채널즈로 복귀한 후 단 3개월 만에 300만을 회복했다고 밝혔다.

Apple TV+ 월간 가입자 분포 분석(2023년 10월 ~ 2024년 12월)을 보면 애플TV(Apple TV+)는 주로 iTunes를 통한 안정적인 가입자 유입을 유지했으나, 2024년 10월부터 아마존 채널스(Amazon Channels)를 통한 신규 가입이 빠르게 증가하며 유통 채널 다각화가 가속화되고 있다. 특히 2024년 12월에는 아마존 채널스(Amazon Channels) 비중이 25%에 달해, 애플 TV플러스(Apple TV+)의 유통 전략 변화와 연말 특수 효과가 뚜렷하게 나타났다.

피콕과 심지어 디즈니의 움직임도 주목해야 할 대목이다. 아마존이 상당한 구독자 증가를 가져다 줄 수 있지만, 구독 수익의 30%-50%를 가져간다는 수수료가 문제다. 그러나 이런 높은 수수료에도 불구하고 더 많은 스트리밍 서비스들이 아마존과의 파트너십을 원하고 있다. 손실보다 이득이 크다는 판단 때문이다.

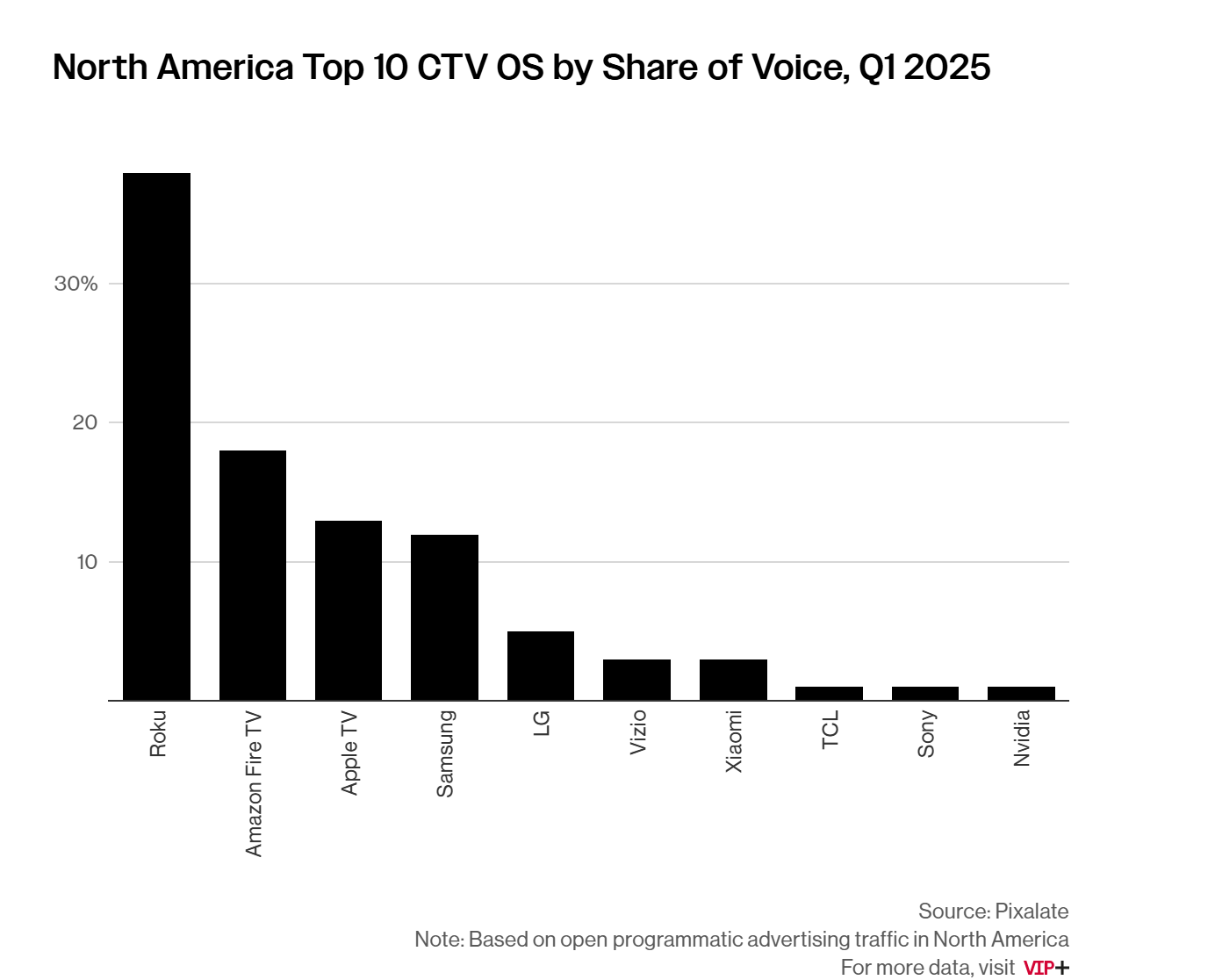

하지만 아마존에게도 강력한 경쟁자들이 있다. 바로 스마트 TV 운영체제(CTV OS)를 만드는 회사들이다. 로쿠(Roku)나 삼성(Samsung) 같은 회사들은 사용자들이 TV를 켤 때 가장 먼저 보는 화면을 제어한다.

이들은 자신들의 플랫폼에서 직접 스트리밍 서비스를 통합하고 관리할 수 있어 큰 장점을 가지고 있다. 아마존도 파이어 TV OS(Fire TV OS)로 이 시장에 참여하고 있지만, 로쿠나 삼성보다는 점유율이 낮은 상황이다.

While this "cable TV plus streaming" bundle strategy is unlikely to ultimately save cable TV's fate, Charter's limited success demonstrates that pay-TV operators with extensive experience in bundling and product launches retain market defense capabilities even in the streaming era.

However, the future looks challenging. Cable TV and satellite broadcasters' financial resources and subscriber bases seem insufficient to compete with Amazon, the "everything store." Amazon's Prime Video Channels service appears destined to become the dominant streaming aggregation platform. Prime Video Channels allows Amazon Prime or Prime Video members to add various premium streaming services like HBO Max, Paramount+, Starz, and Showtime to their Prime Video accounts for additional monthly fees, managing and viewing everything from one location. Even Kocowa, Korea's only global streaming service, is available for subscription through Amazon Channels.

새로운 도전자의 등장: 월마트의 야심찬 진출

오프라인 유통 1위 월마트(Walmart)의 FAST(Free Ad Supported Streaming TV)와 스트리밍 서비스 시장 진출도 새로운 관점 포인트다. 아마존은 이제 "모든 것을 파는 상점" 사업에서의 오랜 경쟁자로부터 새로운 도전에 직면하고 있다. 바로 월마트(Walmart)다. 월마트는 최근 TV 제조업체 비지오(Vizio) 인수를 통해 스트리밍 파워 플레이어로 자리매김하려는 집중적인 노력을 기울이고 있다.

지난 6월 월마트가 중요한 결정을 내렸다. 자사 브랜드인 온라인 스마트 TV에 기존 사용하던 로쿠(Rocku) 운영체제를 빼고, 대신 인수한 비지오(Vizio)의 스마트캐스트 OS(SmartCast OS)를 사용하기로 한 것이다. 이렇게 하면 월마트는 자사 TV의 모든 기능을 직접 관리할 수 있게 된다. 더 중요한 건 고객들이 TV에서 스트리밍 서비스에 가입할 때 월마트가 수수료를 받을 수 있다는 점이다.

사실 더 중요한 사실은 제3자 유통(스트리밍 통합 플랫폼)이 SVOD 사업에서 점점 더 중요해지는 시점에 월마트가 스트리밍 통합 전쟁에 공식적으로 진입했다는 것이다. 버라이즌은 성공하지 못했지만,온라인 유통 위 아마존은 다를 수 있다.

월마트의 '스트리밍 플랫폼' 시장 진입은 의미가 크다. 첫째, 월마트는 이미 수억 명의 고객을 보유한 글로벌 소매 거대 기업이라는 점이다. 이들 고객들은 이미 월마트 생태계에 익숙하며, 새로운 스트리밍 서비스나 번들을 구매하는 것에 대해 상대적으로 거부감이 적을 것이다. 둘째, 월마트는 수십 년간 다양한 제품을 효율적으로 유통하고 마케팅해온 노하우를 보유하고 있다. 이는 복잡한 스트리밍 서비스 포트폴리오를 관리하고 고객에게 어필하는 데 있어 상당한 이점이 될 수 있다.

셋째, 비지오 인수를 통해 월마트는 하드웨어부터 소프트웨어까지 전체 사용자 경험을 통제할 수 있게 되었다. 이는 아마존이나 다른 경쟁사들과 차별화되는 중요한 요소다. 고객이 월마트에서 구입한 TV를 통해 자연스럽게 월마트의 스트리밍 서비스에 노출되고, 이를 통해 추가 구독을 유도할 수 있는 완전한 생태계를 구축할 수 있기 때문이다.

월마트의 전략은 특히 주목할 만하다. 이 회사는 단순히 기존 플레이어들을 모방하는 것이 아니라, 자신만의 독특한 접근 방식을 택하고 있다. 월마트의 거대한 물리적 매장 네트워크와 온라인 플랫폼을 통해 스트리밍 서비스를 홍보하고 판매할 수 있으며, 이는 다른 어떤 경쟁사도 가지지 못한 독특한 유통 채널이다. 또한 월마트 플러스(Walmart+) 같은 기존 구독 서비스와의 번들링을 통해 고객들에게 더 매력적인 패키지를 제공할 수도 있다. 특히 월마트는 자체 무료 스트리밍 서비스인 패스트(FAST, Free Ad-Supported Streaming Television) 플랫폼도 운영하고 있어, 이를 유료 서비스와 함께 묶어서 제공하는 전략도 가능하다.

Amazon's Overwhelming Dominance and Its Implications

At a recent industry event, Amazon revealed research from Antenna that they commissioned. According to this report, subscriptions through Prime Video Channels accounted for approximately 25% of new SVOD subscriptions in the US during Q1 2025. Antenna data shows this makes Amazon the overwhelming leader among third-party distributors, with a larger market share than all major app stores combined, including Apple and Google Play.

Previous Antenna reports indicated that Amazon's advantage primarily came from smaller "niche" SVOD subscription services rather than premium platforms—essentially, people subscribed through Amazon because it offered specialized streaming services unavailable elsewhere. However, the situation has changed. Nevertheless, major streaming services still largely avoid dealing with Amazon. Netflix, Disney+, and even Peacock still don't participate in Prime Video Channels. But things are shifting. Apple TV+'s addition to the Channels lineup demonstrated Amazon's advantage over major Big Tech competitors in the aggregation space.

Apple TV+ saw positive effects from joining Prime Video Channels, with subscribers surging after the partnership. The report also revealed that HBO Max lost approximately 5 million subscribers after terminating its distribution agreement with Prime Video in 2021, but recovered 3 million within just three months of returning to Channels the following year.

Apple TV+ Monthly Subscriber Distribution Analysis (October 2023 - December 2024)

Apple TV+ maintained stable subscriber acquisition primarily through iTunes from October 2023 to September 2024, but starting in October 2024, new subscriptions through Amazon Channels began rapidly increasing, accelerating distribution channel diversification. By December 2024, Amazon Channels accounted for 25% of new subscriptions, clearly demonstrating Apple TV+'s distribution strategy shift and year-end promotional effects.

결론: 새로운 경쟁 구도의 시작

스트리밍 통합 플랫폼 전쟁은 이제 새로운 국면에 접어들었다. 과거 몇 년간 통신 업체와 아마존이 경쟁했지만, 이제는 온라인 유통 빅테크 아마존이 압도적인 우위를 점하며 이 시장을 주도하고 있다. 그러나 이제는 월마트라는 새로운 강력한 도전자가 등장하면서 경쟁 구도가 완전히 바뀔 조짐을 보이고 있다. 차터와 같은 전통적인 케이블TV 사업자들이 어느 정도 성공을 거두고 있는 것은 분명하지만, 이들의 영향력은 여전히 제한적이다.

버라이즌의 철수는 단순히 한 회사의 실패를 넘어서, 통신사들이 스트리밍 생태계에서 주도적 역할을 하기 어려움을 보여주는 대표 사례다. 이는 통신사들이 가진 기술적 인프라와 고객 기반에도 불구하고, 스트리밍 통합이라는 새로운 비즈니스 모델에서는 다른 종류의 전문성과 접근 방식이 필요함을 시사한다.

반면 월마트의 진입은 소매업의 거대한 힘이 스트리밍 시장에서도 발휘될 수 있음을 시사한다. 특히 월마트가 보유한 고객 기반의 규모와 충성도, 그리고 비지오 인수를 통해 확보한 기술적 역량은 기존 플레이어들에게 심각한 위협이 될 것으로 예상된다. 월마트는 또한 가격 경쟁력 면에서도 강점을 가지고 있어, 소비자들에게 더 저렴한 스트리밍 번들을 제공할 수 있을 것이다.

앞으로 스트리밍 통합 시장은 아마존의 독주 체제에서 벗어나 다극 경쟁 구조로 변화할 가능성이 높다. 월마트는 자신만의 차별화된 접근 방식과 기존 소매업에서의 성공 경험을 바탕으로 이 시장에서 상당한 입지를 구축할 것으로 보인다. 이러한 경쟁 심화는 결국 소비자들에게 더 다양한 선택지와 더 나은 서비스, 그리고 더 합리적인 가격을 제공하게 될 것이며, 이는 전체 스트리밍 생태계의 발전에도 긍정적인 영향을 미칠 것으로 전망된다.

주목할 점은 이러한 변화가 단순히 플랫폼 간의 경쟁을 넘어서, 서로 다른 산업 분야의 거대 기업들이 스트리밍이라는 새로운 전장에서 맞붙는 양상으로 발전하고 있다는 것이다. 기술 기업인 아마존, 소매 기업인 월마트, 그리고 통신 기업들 사이의 이러한 경쟁은 앞으로 스트리밍 산업의 미래를 결정짓는 중요한 요소가 될 것이다.

The New Challenger: Walmart's Ambitious Entry

Walmart, the offline retail leader, has entered the FAST (Free Ad Supported Streaming TV) and streaming services market, presenting a new competitive dynamic. Amazon now faces a new challenge from its longtime competitor in the "everything store" business. Walmart is making concentrated efforts to position itself as a streaming power player through its recent acquisition of TV manufacturer Vizio.

In June, Walmart made a crucial decision: removing the Roku operating system from its own-brand online smart TVs and replacing it with Vizio's SmartCast OS. This allows Walmart to directly manage all functions of its TVs. More importantly, Walmart can collect commissions when customers subscribe to streaming services through their TVs.

The more significant fact is that Walmart has officially entered the streaming aggregation war at a time when third-party distribution (streaming aggregation platforms) is becoming increasingly important in the SVOD business. While Verizon failed, Amazon's online retail dominance might be different.

Walmart's entry into the "streaming platform" market is highly significant for several reasons. First, Walmart is a global retail giant with hundreds of millions of customers already familiar with the Walmart ecosystem, making them relatively receptive to purchasing new streaming services or bundles. Second, Walmart has decades of expertise in efficiently distributing and marketing diverse products, providing significant advantages in managing complex streaming service portfolios and appealing to customers.

Third, through the Vizio acquisition, Walmart can now control the entire user experience from hardware to software. This is a crucial differentiating factor from Amazon and other competitors. Customers who purchase TVs from Walmart will naturally be exposed to Walmart's streaming services, enabling the creation of a complete ecosystem that can drive additional subscriptions.

Walmart's strategy is particularly noteworthy. Rather than simply copying existing players, the company is taking its own unique approach. Walmart can promote and sell streaming services through its massive physical store network and online platform—a unique distribution channel no other competitor possesses. Additionally, bundling with existing subscription services like Walmart+ could provide customers with more attractive packages. Walmart also operates its own free streaming service, a FAST (Free Ad-Supported Streaming Television) platform, enabling strategies that bundle free and paid services together.

Conclusion: The Beginning of a New Competitive Landscape

The streaming aggregation platform war has entered a new phase. While telecom companies and Amazon competed over the past few years, online retail giant Amazon now maintains overwhelming dominance in this market. However, the emergence of Walmart as a new powerful challenger suggests the competitive landscape may change completely. While traditional cable TV operators like Charter have achieved some success, their influence remains limited.

Verizon's withdrawal represents more than just one company's failure—it's a representative case showing how difficult it is for telecom companies to play a leading role in the streaming ecosystem. This suggests that despite telecom companies' technical infrastructure and customer bases, streaming aggregation as a new business model requires different types of expertise and approaches.

Conversely, Walmart's entry suggests that retail industry power can be leveraged in the streaming market. Walmart's customer base size and loyalty, combined with technical capabilities secured through the Vizio acquisition, are expected to pose serious threats to existing players. Walmart also has pricing advantages, potentially offering consumers more affordable streaming bundles.

The streaming aggregation market will likely shift from Amazon's dominance to a multipolar competitive structure. Walmart appears positioned to build significant market presence based on its differentiated approach and successful retail experience. This intensified competition will ultimately provide consumers with more choices, better services, and more reasonable prices, positively impacting the overall streaming ecosystem's development.

Particularly noteworthy is how this change extends beyond simple platform competition to different industry giants competing in the new streaming battlefield. The competition between technology company Amazon, retail company Walmart, and telecom companies will be a crucial factor determining the streaming industry's future.

한국에 주는 시사점: 통신사의 한계와 새로운 기회

버라이즌의 실패가 보여주는 통신사의 구조적 한계는 국내 시장에도 중요한 교훈을 제공한다. 오히려 스트리밍 시장에서 주목해야 할 사실은 유통 기업들의 부상이다. 월마트의 성공적인 시장 진입은 국내 유통 플랫폼들에게 새로운 가능성을 열어준다.

가장 주목받는 기업은 쿠팡(Coupang)이다. 이미 쿠팡플레이를 통해 스트리밍 시장에 진출한 쿠팡은 로켓배송으로 구축한 강력한 고객 기반과 월마트와 유사한 유통 노하우를 보유하고 있다. 쿠팡플레이를 넘어 다양한 국내외 스트리밍 서비스를 통합하는 플랫폼으로 확장한다면, 국내 스트리밍 통합 시장의 강자로 부상할 가능성이 높다. 쿠팡이츠, 쿠팡페이 등과의 시너지를 통해 월마트처럼 완전한 생태계를 구축할 수 있다는 점이 강점이다.

전통 유통업체인 이마트와 롯데마트도 기회를 엿볼 수 있다. 이들은 오프라인 매장이라는 물리적 접점과 SSG닷컴, 롯데온 등의 온라인 플랫폼을 동시에 운영하며, 월마트와 유사한 O2O(Online to Offline) 역량을 갖추고 있다. 특히 이마트의 경우 트레이더스, 일렉트로마트 등 다양한 업태를 통해 세분화된 고객층을 확보하고 있어, 이를 활용한 맞춤형 스트리밍 번들 서비스 제공이 가능하다.

또 삼성전자의 스마트 TV OS인 타이젠(Tizen)이나 LG전자의 웹OS(webOS) 같은 국내 기업들의 TV 운영체제도 새로운 기회를 맞을 수 있다. 미국에서 로쿠나 삼성이 스마트 TV를 통해 스트리밍 통합 서비스에서 우위를 점하고 있는 것처럼, 국내에서도 TV 제조사들이 자체 통합 플랫폼을 통해 스트리밍 시장에서 새로운 역할을 할 수 있을 것이다. 물론 삼성과 LG가 힘을 합치는 건 어디까지나 가상 시나리오다.

네이버나 카카오 같은 플랫폼 기업들도 주목해야 한다. 이들이 가진 광범위한 사용자 기반과 다양한 서비스 연결 능력은 스트리밍 통합 플랫폼 구축에 유리한 조건이다. 특히 웹툰, 웹소설, 음악 등 다양한 콘텐츠 서비스를 이미 제공하고 있는 이들 기업들은 스트리밍 서비스까지 통합해 제공할 수 있는 잠재력을 가지고 있다.

Implications for Korea: Telecom Limitations and New Opportunities

Verizon's failure demonstrates structural limitations of telecom companies that provide important lessons for the domestic market. Rather, the key development to watch in the streaming market is the rise of retail companies. Walmart's successful market entry opens new possibilities for domestic retail platforms.

The most notable company is Coupang. Having already entered the streaming market through Coupang Play, Coupang possesses a strong customer base built through Rocket Delivery and retail expertise similar to Walmart's. If Coupang expands beyond Coupang Play to become a platform integrating various domestic and international streaming services, it could emerge as a leader in Korea's streaming aggregation market. The synergy with Coupang Eats, Coupang Pay, and other services could enable building a complete ecosystem like Walmart's.

Traditional retailers E-Mart and Lotte Mart also see opportunities. They operate both physical stores as touchpoints and online platforms like SSG.com and Lotte ON, possessing O2O (Online to Offline) capabilities similar to Walmart's. E-Mart particularly has secured segmented customer bases through various formats like Traders and Electro Mart, enabling customized streaming bundle services.

Samsung Electronics' Tizen smart TV OS and LG Electronics' webOS also face new opportunities. Just as Roku and Samsung gain advantages in streaming aggregation services through smart TVs in the US, domestic TV manufacturers could play new roles in the streaming market through their own integrated platforms. Of course, Samsung and LG collaborating remains a hypothetical scenario.

Platform companies like Naver and Kakao also deserve attention. Their extensive user bases and diverse service integration capabilities provide favorable conditions for building streaming aggregation platforms. These companies already provide various content services like webtoons, web novels, and music, giving them potential to integrate streaming services as well.

![[Report]Inclusion & Equity Report 2025 by WGA](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/05/dza9ol_202505310259.png)

![[Report]라이선싱엑스포 2025 심층 보고서](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/05/srjw47_202505191926.png)