Disney Secures Global Exclusive Streaming Rights to Netflix’s Beloved Kids’ Hit ‘CoComelon’

디즈니(Disney)가 넷플릭스의 대표 유아용 인기작 ‘코코멜론’의 글로벌 독점 스트리밍 권리를 확보했다. 2027년부터 ‘코코멜론’의 모든 시즌은 디즈니+에서만 볼 수 있게 되며, 이 계약은 유아·가족 스트리밍 시장의 경쟁 구도를 근본적으로 흔드는 대형 거래다.

디즈니는 이미 ‘블루이’ 등 강력한 키즈 라인업을 보유한 가운데, ‘코코멜론’까지 품으며 키즈·가족 고객층 점유율을 한층 더 높일 전망이다. 팬덤 충성도가 높은 유아 콘텐츠의 이동은 수천만 달러의 가치와 함께, 글로벌 스트리밍 시장의 판도를 바꿀 결정적 분기점이 될 것으로 보인다.

Disney Secures Global Exclusive Streaming Rights to Netflix’s Beloved Kids’ Hit ‘CoComelon’

Starting in 2027, every season of CoComelon will be available only on Disney+, marking a major deal that fundamentally reshapes the competitive landscape of the family streaming market. Already home to a robust kids’ lineup including Bluey, Disney’s move to add CoComelon further strengthens its foothold in the kids’ and family demographic.

Given the high loyalty and engagement that come with children’s content, the transition of this popular show—together with the investment of tens of millions of dollars—could serve as a major turning point in the global streaming market.

코코멜론, 전 세계적으로 꾸준한 인기

월트 디즈니 컴퍼니(Walt Disney Co.)가 넷플릭스(Netflix)의 대표 유아용 인기작인 ‘코코멜론(CoComelon)’의 독점 스트리밍 권리를 확보했다. 이로써 2027년부터는 ‘코코멜론’의 모든 시즌을 디즈니+에서만 서비스할 예정이다. 블룸버그에 따르면 디즈니는 이 권리를 확보하기 위해 연간 수천만 달러 규모의 금액을 지불하기로 한 것으로 알려졌다.

‘코코멜론’은 주로 영유아를 대상으로 하는 동요·교육용 콘텐츠로, 2006년 유튜브에서 시작되었다. 현재 공식 유튜브 채널은 1억9천만 명이 넘는 구독자를 보유하고 매월 20억 회 이상의 조회수를 기록하며 꾸준한 인기를 이어가고 있다.

2024년 넷플릭스에서 가장 많이 시청된 프로그램 가운데 ‘브리저튼(Bridgerton)’ 시리즈에 이어 2위를 차지할 정도로 큰 화제를 모았다.

넷플릭스 2024년 TOP 10 조회수 (단위: 백만)

브리저튼/퀸 샬럿 █████████████████████████████████████ 240.6

코코멜론 ██████████████████████████████████ 231.1

페파 피그 ██████████████████████████████ 215.7

영 셸든 ████████████████████ 176.8

개비의 돌하우스 ███████████████████ 174.7

댐셀 ███████████████████ 174.1

리프트 ████████████████ 158.8

슈츠 █████████████ 149.5

캐리-온 ████████████ 137.3

더 유니언 ██████████ 131.1

| 순위 | 프로그램/프랜차이즈 | 조회수 (2024년, 백만 단위) |

|---|---|---|

| 1 | 브리저튼/퀸 샬럿 (Bridgerton/Queen Charlotte) | 240.6 |

| 2 | 코코멜론 (CoComelon) | 231.1 |

| 3 | 페파 피그 (Peppa Pig) | 215.7 |

| 4 | 영 셸든 (Young Sheldon) | 176.8 |

| 5 | 개비의 돌하우스 (Gabby's Dollhouse) | 174.7 |

| 6 | 댐셀 (Damsel) | 174.1 |

| 7 | 리프트 (Lift) | 158.8 |

| 8 | 슈츠 (Suits) | 149.5 |

| 9 | 캐리-온 (Carry-On) | 137.3 |

| 10 | 더 유니언 (The Union) | 131.1 |

CoComelon: A Steadily Popular Global Sensation

The Walt Disney Company has secured exclusive streaming rights to CoComelon, Netflix’s flagship children’s show. According to Bloomberg, Disney will pay an annual fee in the tens of millions of dollars, and from 2027 onward, every season of CoComelon will stream exclusively on Disney+.

Originally launched on YouTube in 2006, CoComelon primarily targets infants and toddlers with nursery rhymes and educational content. Its official YouTube channel boasts over 190 million subscribers and garners more than 2 billion views monthly, a testament to its enduring global popularity.

Netflix’s Top 10 Shows in 2024 (in millions of views)

Bridgerton/Queen Charlotte █████████████████████████████████████ 240.6

CoComelon ██████████████████████████████████ 231.1

Peppa Pig ██████████████████████████████ 215.7

Young Sheldon ████████████████████ 176.8

Gabby’s Dollhouse ███████████████████ 174.7

Damsel ███████████████████ 174.1

Lift ████████████████ 158.8

Suits █████████████ 149.5

Carry-On ████████████ 137.3

The Union ██████████ 131.1

넷플릭스에서 디즈니+로, 2027년부터 독점 서비스

이번 계약에 따라 2027년부터는 디즈니+가 ‘코코멜론’ 전 시즌의 글로벌 독점 스트리밍 서비스 권한을 갖는다.

한편 넷플릭스는 현재 서비스 중인 ‘코코멜론 레인(CoComelon Lane)’이라는 오리지널 시리즈와 또 다른 유아용 콘텐츠 ‘블리피(Blippi)’ 등의 작품에 대해서는 계속 스트리밍을 제공할 계획이다.

유아 시장 경쟁력 강화 노리는 디즈니+

디즈니는 이미 호주 애니메이션 ‘블루이(Bluey)’ 등 인기 유아·키즈 콘텐츠를 통해 강력한 가족 대상 라인업을 갖추고 있다.전통적으로 ‘미키 마우스’, ‘인어공주’ 등 클래식 IP(지식재산권)에 강점이 있던 디즈니가, 새롭게 떠오르는 유튜브 기반 콘텐츠까지 확보함으로써 키즈·가족 고객층에 대한 점유율을 더욱 높일 것으로 전망된다.

디즈니+는 2025년 3월 말 기준 1억2,600만 명의 가입자를 확보하고 있으며, 키즈·가족 콘텐츠 강화로 경쟁 서비스와의 차별화를 노리고 있다.

유튜브와 스트리밍 시장, 유아용 콘텐츠 경쟁 치열

최근 유아·아동용 콘텐츠는 넷플릭스, 디즈니+ 등 주요 스트리밍 플랫폼 간 경쟁이 치열해지고 있다. 시청자 층이 어린 만큼 한 번 팬덤이 형성되면 충성도가 높고, 가족 단위로 오랜 기간 구독을 이어가는 경우가 많아 플랫폼 입장에서 가치가 크다.

이번 계약으로 인해, 그동안 넷플릭스에서 주로 시청되던 ‘코코멜론’이 디즈니+의 핵심 키즈 콘텐츠로 자리매김할 전망이다.

문버그(Moonbug)과 캔들 미디어(Candle Media)의 역할

‘코코멜론’은 본래 전직 광고 전문가 제이 전(Jay Jeon)이 창작한 유튜브 채널로 시작되었으며, 이후 영국 소재의 문벅 엔터테인먼트(Moonbug Entertainment)에 인수되었다.

문벅은 이후 전 디즈니 임원진인 케빈 메이어(Kevin Mayer)와 톰 스태그스(Tom Staggs)가 이끄는 캔들 미디어(Candle Media)에 매각되었다.

문벅 측은 이번 디즈니 계약에 대해 공식적으로 언급하지 않았으며, 유튜브 채널은 그대로 운영하면서 디즈니+를 유료 스트리밍 독점 플랫폼으로 삼을 것으로 보인다.

2027년 극장판도 공개 예정

‘코코멜론’은 2027년경 유니버설 픽처스(Universal Pictures)를 통해 극장판 영화로도 개봉할 계획이다. 이로써 극장판과 함께 디즈니+ 스트리밍까지 이어지는 시너지 효과가 기대된다.

이번 ‘코코멜론’ 독점 계약으로 디즈니는 유아·아동 콘텐츠 생태계에서 확고한 입지를 다시 한번 다지게 됐다. 빠르게 성장하는 스트리밍 경쟁 시대에, 키즈 콘텐츠가 가입자 유치 및 유지에 핵심적 역할을 맡고 있다는 점이 다시금 확인된 셈이다. 앞으로 남은 2년여의 기간 동안 ‘코코멜론’ 시청자가 얼마나 디즈니+로 이동할지, 그리고 이를 통해 디즈니가 어떤 시장 반응을 이끌어낼지 주목된다.

CoComelon의 Netflix 시청 시간 변화 (2023~2024년)

| 기간 | 시청 시간 (백만 시간) |

|---|---|

| 2023년 상반기 | 601.2 |

| 2023년 하반기 | 436.8 |

| 2024년 상반기 | 307.6 |

| 2024년 하반기 | 246.9 |

Moving From Netflix to Disney+ in 2027

Under the new agreement, Disney+ will have exclusive worldwide streaming rights to CoComelon beginning in 2027. Meanwhile, Netflix will continue to stream its original series CoComelon Lane as well as other kid-friendly content such as Blippi.

Disney+ Sets Its Sights on Enhanced Kids Market Competitiveness

Disney already boasts a strong family-oriented lineup with shows like the Australian animated series Bluey. The company has historically held a competitive edge in classic IP—think Mickey Mouse and The Little Mermaid—but by adding YouTube-based hits like CoComelon, Disney aims to further solidify its share among kids and family audiences.

As of March 2025, Disney+ reported 126 million subscribers. The company intends to leverage children’s and family programming to differentiate itself from competing services and broaden its subscriber base.

Fierce Competition in the YouTube and Streaming Markets for Children’s Content

Competition for children’s content among major platforms (Netflix, Disney+, and others) has intensified. Since kids’ loyalty tends to be high once they latch onto a show—and because families may keep a subscription long-term—children’s content is considered highly valuable.

Disney’s acquisition of CoComelon, previously a mainstay on Netflix, is poised to establish the show as a key pillar of Disney+’s kids’ offering.

The Role of Moonbug and Candle Media

CoComelon was initially created as a YouTube channel by former advertising executive Jay Jeon. It was acquired by the UK-based Moonbug Entertainment, which was later purchased by Candle Media, a firm led by ex-Disney executives Kevin Mayer and Tom Staggs.

Though Moonbug declined to comment on the Disney deal, it is expected that CoComelon will remain available on YouTube, with Disney+ becoming its exclusive paid streaming platform.

Movie Adaptation Slated for 2027

A CoComelon feature film is planned for theatrical release by Universal Pictures around 2027. Disney+’s streaming deal, combined with a full-length movie in theaters, is anticipated to generate synergistic effects, drawing even more attention to the brand.

With this exclusive agreement, Disney further cements its position in the children’s content ecosystem. As the competition among streaming services accelerates, it underscores the critical role that kids’ programming plays in subscriber acquisition and retention. Over the next two years, the industry will watch closely to see how many of CoComelon’s fans migrate to Disney+ and how Disney capitalizes on this strategic bet.

한국에 주는 메시지

최근 국내에서도 넷플릭스, 디즈니+, 웨이브(Wavve), 티빙(TVING) 등 다양한 스트리밍 플랫폼이 경쟁을 벌이고 있으며, 유아·어린이 콘텐츠에 대한 수요가 꾸준히 증가하고 있다. 전 세계적으로 성공한 ‘코코멜론’의 디즈니+ 독점 행보는 한국 시장에도 다음과 같은 시사점을 준다.

스트리밍 경쟁 심화와 맞춤형 전략 필요

유아·가족 대상 콘텐츠는 가입자 충성도가 높아, 장기적으로 플랫폼에 머무를 가능성이 크다.국내 스트리밍 업체들도 글로벌 IP(지식재산권)와 협업하거나 자체 키즈·애니메이션 콘텐츠 확보에 집중해야 한다는 목소리가 높다.

캐릭터·콘텐츠 산업에 새로운 기회

‘코코멜론’ 같은 글로벌 흥행작이 디즈니의 자본과 마케팅으로 더욱 성장하듯, 한국 애니메이션 및 캐릭터들도 세계적 플랫폼과 협업해 성장할 가능성이 높아진다. 국내 제작사와 스튜디오들은 글로벌 시장 진출을 염두에 두고 콘텐츠 기획·제작 단계부터 해외 유통 전략을 고민해야 한다.

What This Means for the Korean Market

In South Korea, where Netflix, Disney+, Wavve, and TVING all compete, demand for children’s content is continually growing. The global success and exclusive move of CoComelon to Disney+ highlights several key takeaways for the Korean market:

Escalating Streaming Competition and the Need for Targeted Strategies

Children’s and family content often secures high subscriber loyalty, encouraging longer-term platform engagement. Korean streaming services should consider partnering with global IP holders or creating their own kids’ and animated content to remain competitive.

New Opportunities for the Character and Content Industries

Just as CoComelon has expanded with Disney’s capital and marketing support, Korean animation and character properties could find similar opportunities for global growth through major platform collaborations. From the earliest stages of planning and production, domestic studios should strategize for international distribution and partnerships.

Establishing a Family-Friendly Streaming Environment

Parents want safe, high-quality educational and entertainment options for their children. By bolstering robust kids’ content, Disney+ has succeeded in attracting families. Korean platforms should likewise focus on curated children’s channels, parental controls, and high-quality family content.

Ultimately, the shift of CoComelon from Netflix to Disney+ illustrates how pivotal kids’ programming has become in the fiercely competitive OTT market. For Korean content creators and streaming platforms, the emphasis on discovering, developing, and globalizing engaging children’s programming has never been more crucial.

어린이·가족 콘텐츠에 주목하는 스트리밍

디즈니와 사례와 같이 많은 스트리밍 서비스들이 어린이·가족 대상 프로그램을 대거 확보하거나 확장 중이다. 이는 SVOD(유료 구독형)부터 FAST(무료 광고 기반 스트리밍 TV)까지 전방위적으로 나타나는 현상이다. 가족 단위 시청이 시청 시간(engagement)과 광고 효율을 높이고, 구독 이탈(churn)을 줄이는 효과가 있다는 연구 결과가 잇따라 나오면서, 기존 서비스들은 어린이 콘텐츠 확보에 박차를 가하고 있다.

디즈니+: 대표적인 가족·어린이 콘텐츠 강자로 인식돼 왔지만, 최근 그 외 스트리머들도 대규모 라이선스를 통해 라이브러리를 확충하고 있다.

아마존 프라임 비디오: 어린이 콘텐츠 비중이 그리 높지 않아 보이지만, 절대적인 타이틀 수에서 가장 큰 규모를 보유하고 있으며, 글로벌 배급 측면에서도 선두권에 있다.

FAST 플랫폼: 대표적으로 플루토TV(Pluto TV), 로쿠(Roku), 투비(Tubi) 등은 저예산·기존 IP 라이선스를 통해 어린이·가족 콘텐츠 카탈로그를 급증시키고 있다.

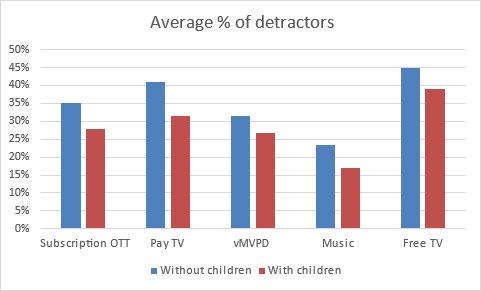

1. 어린이 시청층이 구독 해지를 줄인다

어린이 있는 가정, ‘구독 지속률’ 높다

시장조사업체 앰피어 애널리시스(Ampere Analysis)의 2024년 9월 조사에 따르면, 어린이가 있는 가정에서 SVOD 서비스를 해지할 확률은 없는 가정 대비 확연히 낮다고 한다. 어린이가 없는 가정은 평균 35%가 구독 해지 위험군으로 분류되지만, 어린이가 있는 가정은 28%에 불과했다.

유료 구독 뿐 아니라 무료 서비스(FAST, AVOD 등)에서도 비슷한 경향:

어린이 없는 가정은 45%가 해지 위험군

어린이 있는 가정은 39%

이는 광고 기반 서비스에서도 가족 시청층이 더 안정적인 유저층임을 시사한다.

암페어 리서치 매니저인 올리비아 딘(Olivia Dean)은 “어린이·가족 콘텐츠가 시청 시간에서 차지하는 비중이 크기 때문”이라며, 부모들은 본인 오락뿐 아니라 아이들의 엔터테인먼트까지 고려해 스트리밍 서비스를 해지하지 않는 경향이 있다고 설명했다.

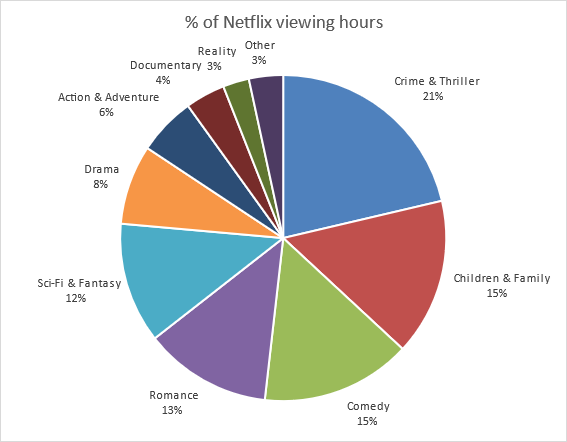

넷플릭스 사례: ‘어린이·가족’ 카테고리가 큰 비중

암페어가 공유한 데이터에 따르면, 2023년 기준 넷플릭스(미국) 시청 시간에서 어린이·가족 콘텐츠가 두 번째로 많이 본 카테고리였다고 한다(1위: 범죄·스릴러, 3위: 코미디). 전 세계 시청 시간 대비 약 15%가 어린이·가족 장르였다.

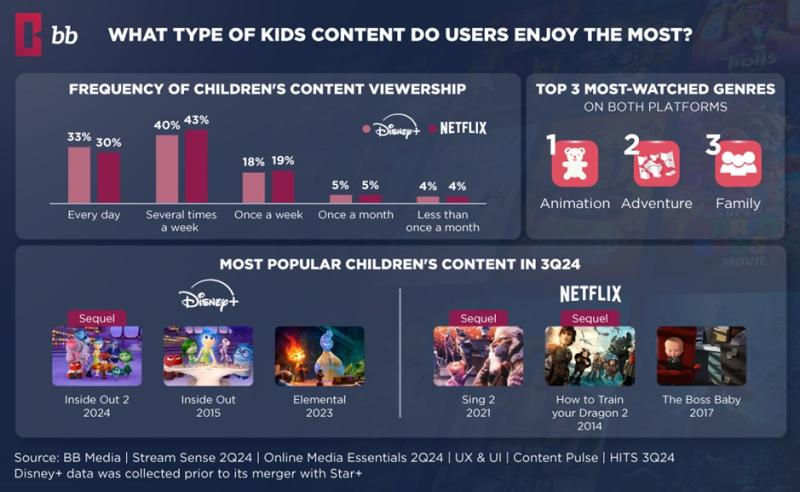

2. ‘키즈’가 핵심인 디즈니+ vs. 넷플릭스의 다면 전략

BB 미디어(BB Media)는 2024년 12월, 라틴아메리카 지역 넷플릭스와 디즈니+를 비교 분석했다. 이 연구에 따르면:

디즈니+: 가족용 콘텐츠가 주 구독 이유. 라틴아메리카 시청자들은 ‘어린이·가족’ 작품 때문에 디즈니+를 선택하는 경우가 매우 높았다.

넷플릭스: 어린이·가족 장르는 중요한 요소이지만, 구독 결정에서 “여러 이유 중 하나”에 불과했다.

두 서비스 모두 어린이 콘텐츠가 “가족 단위의 선택과 플랫폼 충성도(로열티)를 형성하는 핵심”으로 작용하며, 이를 유지하기 위해선 지속적으로 새로운 작품, 사용자 편의 기능(키즈 프로필, 콘텐츠 필터 등)**을 강화해야 한다고 BB 미디어는 강조했다.

3. 오리지널 제작 감소, 기존 IP가 강세

어린이 오리지널 제작 줄어… 라이선싱 시장 ‘활황’

암페어에 따르면, 2022년~2023년 동안 전 세계 오리지널 콘텐츠 제작이 전반적으로 둔화됐는데, 특히 어린이·가족 장르가 세 번째로 큰 타격(작품 수 15% 감소)을 입었다. 그러나 기존 작품 라이선스나 재탕(Non-Original) 콘텐츠는 오히려 4% 증가하여, 스트리밍 서비스들이 기존 인기 IP를 재확보하는 경향이 두드러졌다.

예: 코코멜론(CoComelon), 페파피그(Peppa Pig) 등 넷플릭스에서 큰 인기를 끄는 어린이 라이선스 작품.

앰피어는 “기존 인기 IP를 기반으로 한 작품을 확보한 기업이 치열한 인수 시장에서 유리하다”고 분석한다. 실제로 2024년 상반기에 발표된 어린이 타이틀 중 50%가 기존 시리즈의 후속편이었다.

유명 IP를 기반으로 한 사례

매텔(Mattel)과 아드만(Ardman)의 협력: 핑구(Pingu) 애니메이션 시리즈를 스톱모션 형태로 공동 개발해 여러 플랫폼에 판매할 예정이다.

매텔의 자체 FAST 채널: ‘Barbie and Friends’ 채널, 이어서 ‘Hot Wheels Action’ 채널 론칭 등 장난감 브랜드가 직접 OTT 영역에 진출.

4. 아마존 프라임 비디오가 글로벌 ‘어린이 콘텐츠’ 최다 배급

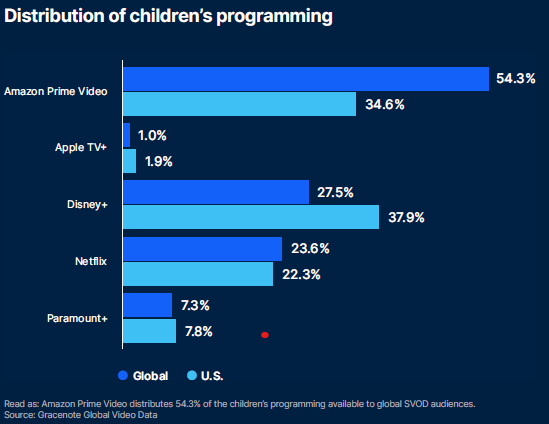

그레이스노트(Gracenote)의 ‘State of Play’ 보고서에 따르면, 전 세계 SVOD에서 유통되는 프로그램 중 11.6%가 어린이 장르다. 여기서 눈에 띄는 점은:

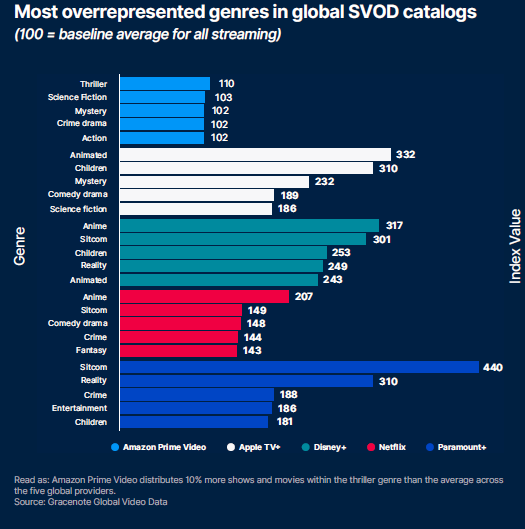

아마존 프라임 비디오가 절대적인 어린이 타이틀 수에서 가장 많은 프로그램을 보유·배급 중이다(글로벌 기준).

디즈니+는 전체 카탈로그 중 어린이·애니메이션 비중이 매우 높지만, 전 세계적으로 보면 프라임 비디오가 더 많은 타이틀을 유통한다는 점이 의외.

미국 내만 보면, 디즈니+가 제공하는 어린이 콘텐츠 비중이 38%로 가장 높다.

넷플릭스는 개별 에피소드 기준으로 보면 디즈니+보다 많은 편수를 제공하는 경우도 있다는 분석.

5. FAST & AVOD도 어린이·가족 콘텐츠 경쟁 치열

앰피어의 2024년 9월 집계에 의하면, 비오리지널 어린이 콘텐츠 확보 경쟁은 FAST(무료 광고 기반)와 AVOD(광고 기반 주문형 비디오)에서 특히 활발하다.

피콕(AVOD 부문): 9월 한 달 동안 707개의 비오리지널 어린이 타이틀 추가

아마존 프라임 비디오: 445개 타이틀 추가

플루토TV(Pluto TV): 368개, 로쿠(Roku): 233개, 투비(Tubi): 147개 등.

이들 무료 플랫폼은 “대량의 키즈 타이틀 확보 → 광고 매출 증대”라는 전략을 취하며, 1년 새 어린이·가족 장르의 타이틀 수가 크게 늘었다. 대표적으로 **투비(Tubi)**는 6,977편으로 전체 플랫폼 중 가장 많은 키즈·가족 작품을 보유하고 있다.

양적 성장과 함께 ‘브랜드 아이덴티티’ 중요

다만, 단순한 타이틀 수(볼륨)만이 승부처는 아니라는 지적이 있다. 디즈니처럼 오래된 상징적 IP를 보유하고 있거나, 매텔처럼 어린이 대상 IP를 장난감·영화·애니메이션으로 확장할 수 있는 브랜드 파워가 결국 승리 열쇠로 작용한다.

6. 어린이·가족 콘텐츠, 광고 효과와 참여도(engagement) 높여

동반 시청(Co-viewing)의 힘

가족 콘텐츠는 자녀와 부모가 함께 시청하는 경향이 커, 광고 참여도 역시 높아진다. AVOD 서비스 퓨처투데이(Future Today)의 조사(2024년 여름)에 따르면:

광고 시청 태도: 가족 시청 시, 광고를 함께 보며 대화를 나누는 확률이 높아지므로 브랜드 인지도와 구매 연계 효과가 증가한다.

응답자 92%는 성인을 위한 광고가 어린이 콘텐츠에 삽입될 때도 주목도가 높았다고 답했다.

‘가족 토론’ 유도: 아이들이 광고를 보며 부모에게 질문하거나 의견을 말하는 과정을 통해 브랜드가 더 각인되는 현상이 생긴다.

퓨처투데이 공동창업자 비크란트 마투르(Vikrant Mathur)는 “어른만 시청할 때는 광고 시간에 자리를 뜨거나 스마트폰을 보는 경우가 흔하지만, 아이들과 함께 볼 때는 광고도 대화 주제가 되어 브랜드에 대한 기억이 강화된다”고 강조했다.

‘Pester Power’: 아이가 부모의 소비 결정에 영향

약 9/10의 어린이들이 본 광고에 대해 이야기하며, 92%는 광고에 나온 제품을 사달라고 요청하는 경우가 있다.

부모들은 아이의 의견을 완전히 무시하기 어렵다. 외식, 여행 등 가족 활동에서 아이의 선호가 중요한 역할을 하는데, 이는 가족 대상 광고가 직접적인 구매 전환으로 이어질 수 있음을 의미한다.

7. 결론: 어린이·가족 콘텐츠, 스트리밍 서비스의 미래 전략

구독 유지(Churn 감소): 어린이 있는 가정이 그렇지 않은 가정보다 스트리밍 서비스를 해지할 가능성이 낮다는 통계는 이미 여러 곳에서 입증.

광고 매출 증대: 동반 시청이 높아지고, 브랜드에 대한 대화·인지도가 상승해 광고주 유치가 용이.

IP 확장·콜라보: 기존 인기 IP(디즈니, 매텔 등) 재활용, 새롭게 라이선싱하거나 후속편 제작 시 성공 가능성이 큼.

FAST와 SVOD 모두에게 기회: 글로벌 오리지널 생산이 줄어든 상황에서, 이미 검증된 키즈 프로그램 확보 경쟁이 치열해질 전망.

어린이·가족 콘텐츠는 ‘단순 어린이 타깃’에 그치는 것이 아니라, 가족 전체를 플랫폼에 묶어두는 효과가 있다는 점에서 앞으로도 스트리밍 시장의 핵심 전략으로 자리잡을 것으로 보인다.

Disney’s 2016 animated film Moana became the most-streamed movie of 2023, and its recently released sequel, Moana 2, broke box office records last month. On YouTube, kids’ content sensation Ms. Rachel was among the top CTV channels in 2024, and is emerging as this holiday season’s hottest new toy license. Meanwhile, popular preschool favorites CoComelon and Peppa Pig dominated Netflix’s list of most-watched licensed TV shows in the first half of 2024. Across the board, kids and family programming is proving essential for streaming platforms—helping to drive viewership and engagement, reduce churn, and deliver strong returns for advertisers.

1. Why Streaming Platforms Are Focusing on Kids & Family Content

Throughout 2024, many OTT services—ranging from paid SVODs to free, ad-supported TV (FAST)—have expanded their children’s and family content. This shift is partly due to research showing that family-oriented programming can increase watch time and enhance subscriber loyalty. For ad-supported services, co-viewing (where kids and adults watch together) can boost ad impact and bolster brand recall.

Disney+: Long recognized for its robust library of family content, but facing new competition from rival platforms aggressively licensing popular kids’ IP.

Amazon Prime Video: Holds a massive overall catalog, including one of the largest global inventories of children’s programs.

FAST Services: Examples include Pluto TV, The Roku Channel, and Tubi, all of which rapidly added kid-friendly and family-safe titles to grow ad revenue and draw in family audiences.

2. Households with Children Have Lower Churn Rates

Ampere Analysis: Families Are More Likely to Keep Their Subscriptions

Research from Ampere Analysis (Q3 2024) shows that households with children are significantly less likely to cancel (churn from) a streaming service:

No Kids in Household: Average 35% churn risk for SVOD

Kids in Household: 28% churn risk

A similar pattern holds true for free, ad-supported services, where churn risk is 45% for child-free homes but only 39% for families with kids.

According to Olivia Dean, Research Manager at Ampere Analysis, “Kids & family content tends to represent a high share of a household’s total watch time when children are present,” motivating parents to maintain subscriptions.

Kids & Family Is a Major Viewing Category on Netflix

Ampere data indicates that in 2023, Children & Family was the second-most watched category on Netflix in the U.S. (surpassed only by Crime & Thriller). Globally, kids & family titles constituted around 15% of Netflix’s total viewing hours. This underscores the sizable impact of kid-oriented programs on a service’s overall audience retention.

3. Disney+ vs. Netflix: Different Approaches to Children’s Content

BB Media’s December 2024 study comparing Disney+ and Netflix in Latin America found:

Disney+: Family-friendly programming is the top reason subscribers join.

Netflix: Offers strong children’s content but treats it as one among several reasons to subscribe.

Both services see family-oriented shows as key to subscriber loyalty, though each employs distinct strategies. Disney+ leans heavily on its iconic IP, while Netflix focuses on diversifying across multiple genres.

4. Original Production Slowdown Favors Existing IP

Reduced Commissions, Stronger Demand for Licensed Titles

Between 2022 and 2023, global production of new original titles slowed significantly, with the kids/family genre down 15%. However, the total number of licensed or non-original children’s shows rose by 4% in the same period. As a result, streaming platforms are clamoring for established and reliable properties:

Popular licensed kids’ shows such as CoComelon and Peppa Pig have performed extremely well on Netflix.

50% of newly announced children’s titles in the first half of 2024 were renewals of existing series.

Existing Brands: A Strategic Edge

Ampere Analysis notes that “services with popular IP have an advantage” in a busy acquisition landscape. Mattel, for instance, has expanded into streaming with dedicated Barbie and Hot Wheels channels, leveraging its well-known toy franchises for additional media revenue.

5. Amazon Prime Video Leads in Global Distribution

According to Gracenote’s “State of Play” report:

Children’s programming makes up 11.6% of total global SVOD content.

Amazon Prime Video has the largest overall volume of kids’ content distributed worldwide, though not the highest proportion relative to its entire library.

Disney+ features a higher share of kids/family content in its catalog (153% above the five-service average), but overall, Amazon carries more titles when viewed on a global scale.

6. FAST & AVOD Services’ Rapid Growth in Kids & Family

Data from Ampere shows that in September 2024 alone:

Peacock (AVOD tier) added 707 children’s/family titles.

Amazon Prime Video added 445.

Pluto TV (FAST) added 368, The Roku Channel 233, Tubi 147, Sling Freestream 137, and Plex 122.

Moreover, from September 2023 to September 2024:

AVOD/BVOD platforms in the U.S. increased kids/family titles by thousands, going from ~16,000 to 22,185 distinct titles.

SVOD platforms grew from 11,640 to 13,195 titles in the same category.

Tubi now leads in raw number of kid/family titles (6,977), followed by Prime Video, Pluto TV, Roku, and Plex. Meanwhile, Disney+ is recognized for quality and iconic IP, even if its raw volume is smaller.

7. Family Programming Drives Ad Engagement

Co-Viewing & “Pester Power”

When kids and parents watch together, ad engagement tends to rise. A summer 2024 study by AVOD player Future Today found that:

92% of parents and 87% of kids stay “net engaged” when an adult-focused ad appears during co-viewing.

Children often ask questions or comment on the ads, turning commercials into conversation starters, which increases brand recall.

9 in 10 kids discuss the ads they see, and 92% at least sometimes ask parents to buy the advertised product.

Future Today co-founder Vikrant Mathur noted that co-viewing changes the dynamic around ad breaks, as parents are less likely to leave the room or tune out when children are present. This environment leads to higher brand trust and more frequent follow-up actions (e.g., in-store visits or online searches).

8. Conclusion: A Core Strategy for Streamers

Kids and family content is poised to remain a critical pillar for streaming services. The benefits are multi-fold:

Churn Reduction: Households with children unsubscribe less frequently.

Advertising Upside: Family co-viewing drives ad engagement and brand discussion.

IP Expansion: Existing brands (Disney, Mattel, etc.) can leverage their classic characters to stay competitive in a crowded market.

FAST & SVOD Alike: Both subscription-based and ad-supported models are ramping up acquisitions of children’s shows, filling a gap left by the slowdown in original production.

Whether they’re building entire channels around beloved franchises or simply acquiring fan-favorite cartoons, streamers see kids & family programming as a reliable engine for viewership, ad revenue, and subscriber loyalty. In other words, it’s “for the kids,” but it also safeguards the bottom line.

![[보도자료]Kocowa, 유럽 진출 1년 성과](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/07/d4i5qa_202507142153.png)

![[Report]Inclusion & Equity Report 2025 by WGA](https://storage.googleapis.com/cdn.media.bluedot.so/bluedot.kentertechhub/2025/05/dza9ol_202505310259.png)