스트리밍 서비스 시즌 1의 싸움이 점유율 경쟁이었다면 스트리밍 2.0에서의 경쟁의 룰은 바로 ‘충성도 높은(engagement) 고객’을 확보하는 것이다. 이들이 플랫폼에 내에 오랫동안 머무는 동시에 덤 많은 상품이나 서비스를 이용할 가능성이 크기 때문이다.

넷플릭스가 팬들을 구독자로 전환시킬 팟캐스터와 유튜버 영입 경쟁에 나섰다. 블룸버그는 넷플릭스가 팟캐스트에 관심을 보이며 관련 콘텐츠를 끌어모으고 있다고 보도했다. 사실 넷플릭스가 유튜브(YouTube)를 타겟팅하는 것은 새로운 일은 아니다.

이 회사는 이미 코코멜론(CoComelon)및 사이드멘(The Sidemen)과 같은 대형 유튜브(YouTube)크리에이터와 계약을 체결한 바 있다. 얼마 전에는 미스 레이첼과 계약을 체결하고 미스터비스트의 TV 프로그램 판권 입찰에 참여했다. 라이브 핫 원(live Hot Ones)에 대한 콘텐츠 계약도 논의되고 있다.

If the battle of streaming services season 1 was about share, the rules of the game in streaming 2.0 are about creating "engaged" customers.

This is because they are more likely to stay on the platform for a longer period of time and take advantage of additional products and services.

Netflix is in a race to sign podcasters and YouTubers to convert fans into subscribers. Bloomberg reports that Netflix is showing interest in podcasts and attracting related content. Netflix's targeting of YouTube is nothing new.

The company has already signed deals with big YouTube creators like CoComelon and The Sidemen. It recently signed a deal with Miss Rachel and bid for the TV rights to Mr. Beast's show. A content deal for a live Hot Ones is also being discussed.

스트리밍 서비스들이 팟캐스터와 유튜버 등 이른바 크리에이터에 뜨거운 구애를 보내고 있다. 시장 초기 유튜버들은 유료 스트리밍에서 성공하지 못했지만, 지금은 상황이 다르다. 크리에이터들은 유료 스트리밍에 구독자를 끌어모이고 유지시킨다. 아마존은 미스터 비스트의 ‘비스트 게임(Beat Game) 시즌2를 확정했다.

요즘 제작비가 오르고 있지만 아직까지 크리에이터 콘텐츠는 고예산 TV프로그램과는 달리 상대적으로 제작비가 저렴하다. 아울러 팟캐스터는 최근 스트리밍 서비스들이 원하는 ‘라이브 프로그램’에 적합하다.

Streaming services have been courting so-called creators, including podcasters and YouTubers. While YouTubers in the early days of the market were not successful in paid streaming, the situation is different now. Creators are attracting and retaining subscribers to paid streaming. Amazon has just renewed Mr. Beast's "Beat Game" for a second season.

While production costs are rising, creator content is still relatively inexpensive to produce, unlike big-budget TV shows. Podcasters are also a great fit for the "live programming" that streaming services are looking for these days.

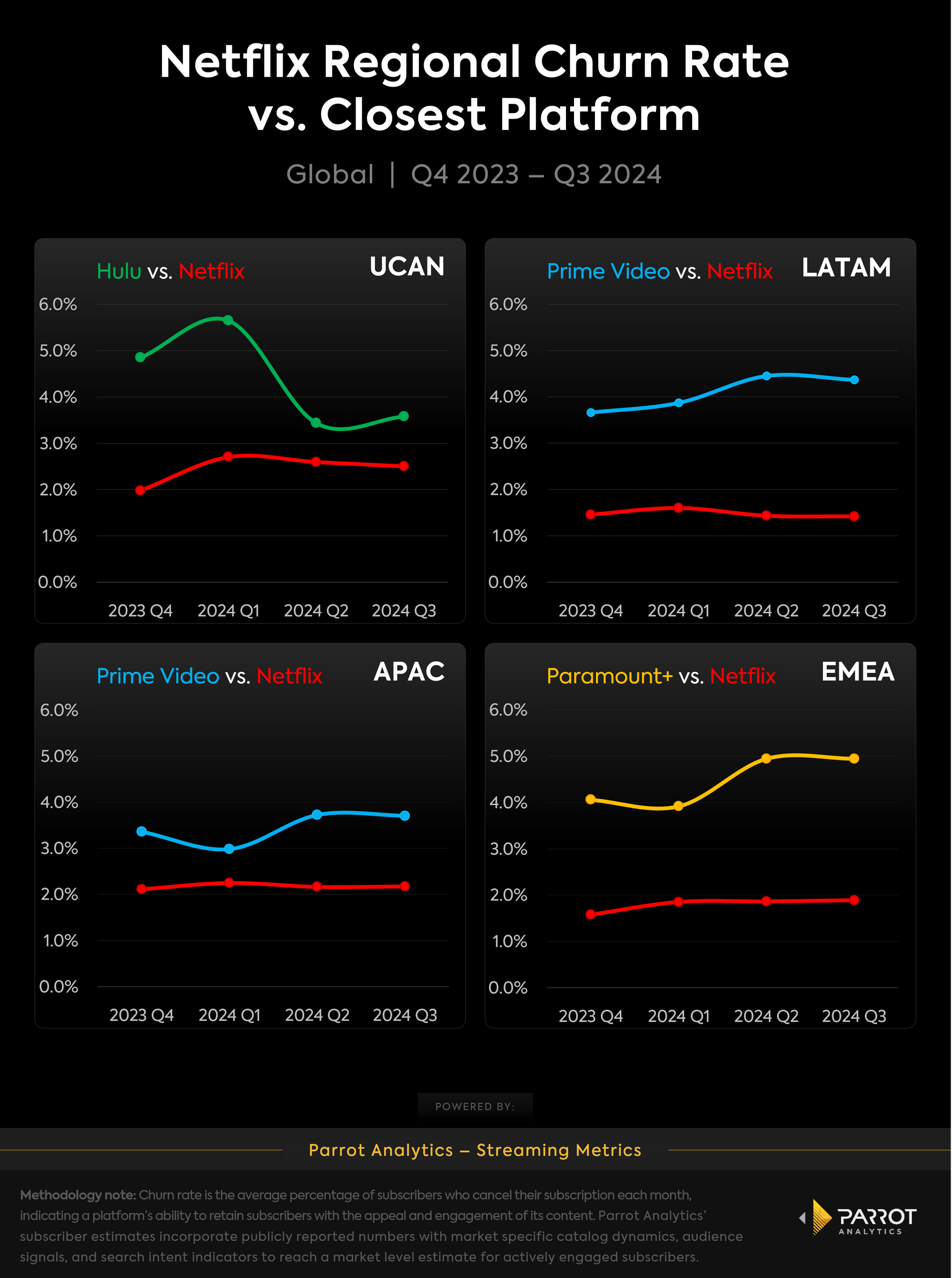

넷플릭스 등 스트리밍 서비스들이 크리에이터에 구애하는 이유는 ‘스트리밍 서비스 점유율 경쟁’이 사실상 끝났기 때문이다. 일반적인 프리미엄 콘텐츠로는 도저히 추가 구독자를 확보하기 어려운 상황이다.

사실 크리에이터 확보 필요성은 넷플릭스보다 다른 사업자에 더 크다.

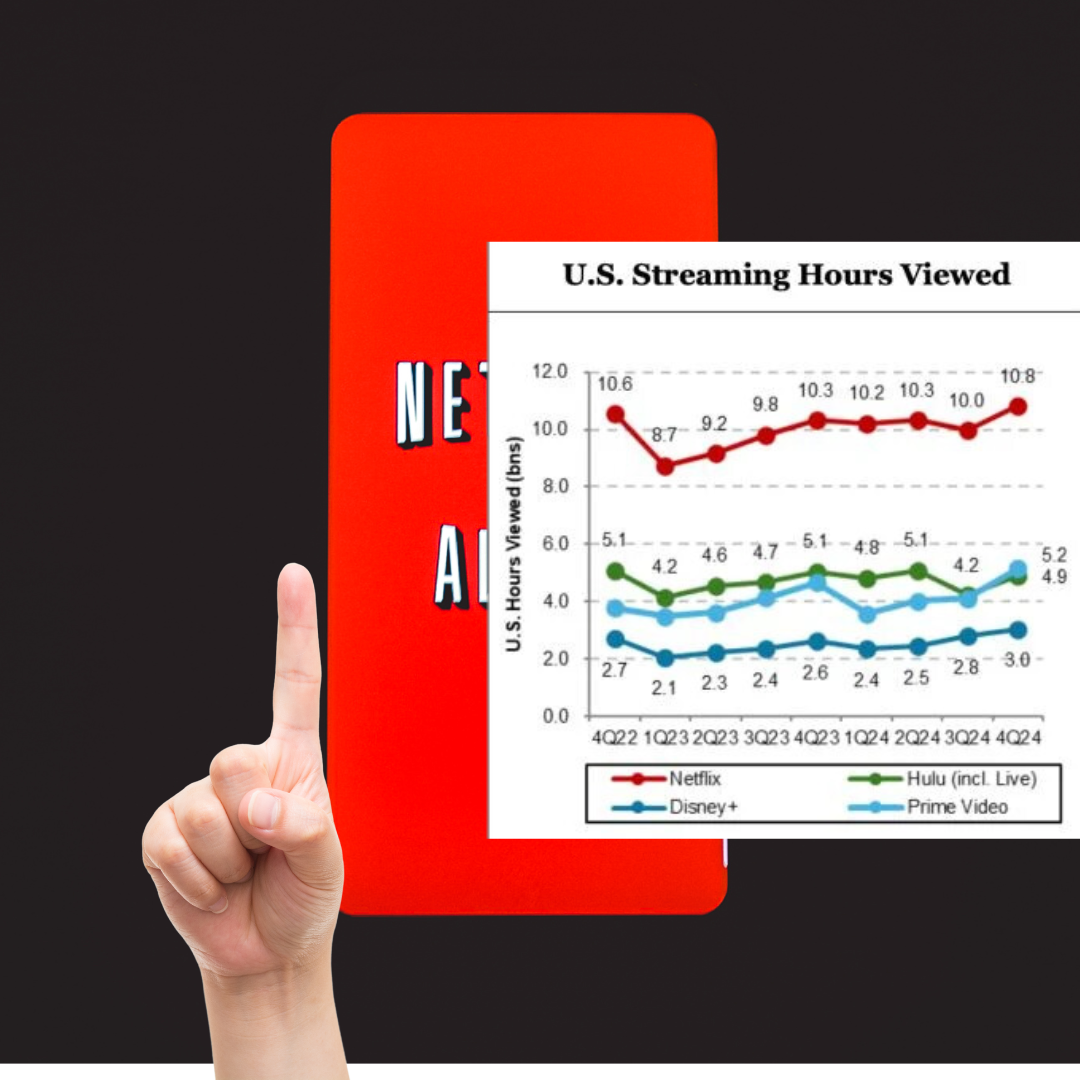

리서치 회사 모펫내탄슨은 보고서(U.S. Media: Streaming Scale Matters)에서 이제 구독 스트리밍 시장 경쟁’은 끝났다고 선언했다. 미국 SVOD의 경우 "전반적으로 참여율 증가세가 둔화돼 해당 밴드 내 자리를 차지하기 위한 경쟁이 벌어지고 있지만, 어떤 서비스도 위나 아래로 도약하지 못하고 있다"라고 말했다

모펫내탄슨은 "미국의 주요 구독 스트리밍 간 스트리밍 패러다임은 굳어졌다(The streaming paradigm has been established)”고 말했다. 2023년부터 2024년까지 미국에서 평균 구독자당 소비 시간은 거의 제자리걸음을 했다.

점유율 고착화를 벗어나기 위해선 M&A나 구독자 규모를 드라마틱하게 늘려야한다.

그러나 M&A나 규모 확대를 위해선 엄청난 콘텐츠 투자가 필요하다. 하지만, 대부분 규모가 작은 사업자는 이를 감당할 돈이 없다.

빈곤의 악순환은 이 지점에서 펼쳐진다.

아무리 열심히 해도 뛰어넘을 수 없는 상황. 힘을 합쳐도 1등 근처에도 못하는 세상이 지금 스트리밍 시장이다.

한국 역시 티빙과 웨이브가 합병을 논의하고 있지만, 글로벌 시장에서는 역부족이다.

The reason Netflix and other streaming services are courting creators is that the race for streaming service share is effectively over. It's no longer enough for them to attract additional subscribers with standard premium content.

In fact, the need to acquire creators is greater for other providers than it is for Netflix.

Research firm MoffettNathanson declared in a report (U.S. Media: Streaming Scale Matters) that the subscription streaming race is over.

For U.S. SVOD, "overall engagement growth has slowed, creating a jockeying for position in the band, but no service is leapfrogging up or down."

"The streaming paradigm has been established among the major subscription streams in the U.S.," Moffett-Natanson said. From 2023 to 2024, average time spent per subscriber in the U.S. was nearly flat.

Breaking out of share lock-in will require M&A or dramatic subscriber growth.

However, M&A and scale require significant content investment. Most smaller operators don't have the money to do this.

This is a vicious cycle of poverty in the streaming market.

넷플릭스는 가장 저렴한 서비스?

모펫내탄슨 보고서에 따르면 넷플릭스는 시청 시간당 가장 적은 금액의 수익(revenue per hour spent viewing)을 올리고 있었다.