미국 위성 방송 디렉TV(DirecTV)가 전통적인 위성 방송사의 이미지를 지워내고, 본격적으로 앱 기반 스트리밍으로 무게중심을 옮기고 있다. 2019년 이후 위성 발사를 중단한 데 이어, 최근에는 ‘DirecTV Stream’ 브랜드를 단계적으로 폐지하고 모든 트래픽을 DirecTV.com으로 일원화하는 등 대대적인 변화를 추진 중이다.

사모펀드 TPG 주도 하의 구조조정과 함께, 농촌 지역을 제외한 대다수 고객에게는 인터넷 스트리밍을 권장하는 전략이 가시화되고 있다.

DirecTV is shedding its traditional image as a satellite broadcaster and pivoting aggressively toward app-based streaming. After halting new satellite launches in 2019, the company is now phasing out the “DirecTV Stream” brand and consolidating all web and mobile traffic under DirecTV.com.

Guided by private equity firm TPG, DirecTV is restructuring its services to steer most customers in urban areas toward internet streaming, keeping satellite TV primarily for rural regions with limited broadband access.

디렉TV의 새 전략: 위성에서 스트리밍으로

디렉TV(DirecTV)는 “DirecTV Stream” 브랜드를 단계적으로 없애면서 웹·모바일 트래픽을 모두 DirecTV.com 메인 페이지로 통합하고 있다. 이는 위성 중심 서비스에서 스트리밍 중심으로 빠르게 전환하기 위한 움직임으로 볼 수 있다.

DirecTV’s New Strategy: Moving From Satellite to Streaming

DirecTV (DirecTV) stopped launching new satellites in June 2019 and has since begun phasing out the “DirecTV Stream” label, directing all website and mobile traffic through DirecTV.com. This shift signals a broader push away from satellite-focused services and toward app-based streaming.

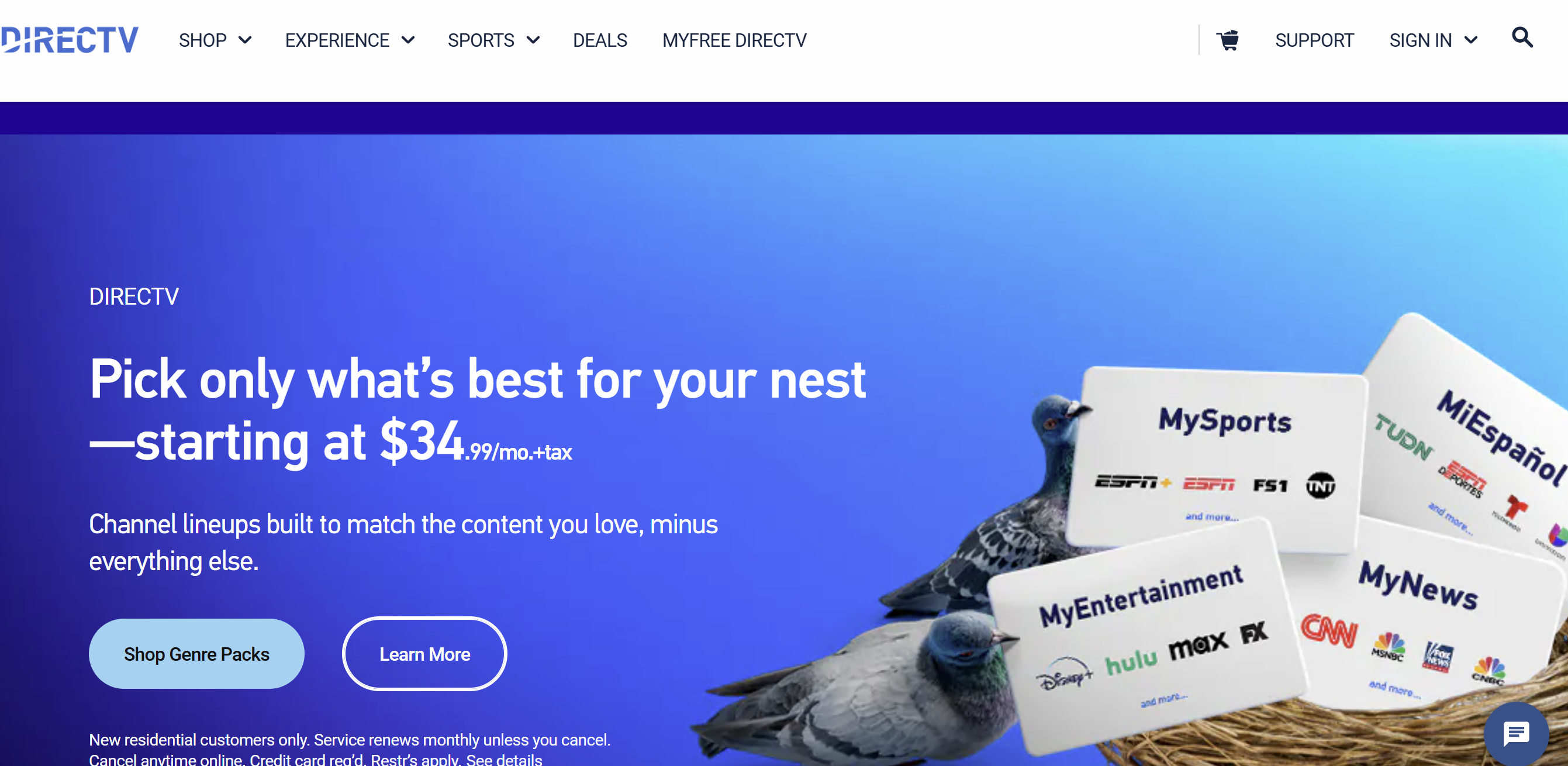

1. 새롭게 정비된 상품 구조

1) MyFree DirecTV(FAST 채널)

출시 시기: 2022년 10월

특징: 100개 채널을 무료 광고 기반(FAST)으로 제공

이용 방법: 별도 가입 없이 DirecTV 앱에서 무료 시청 가능

2) 장르별 상품(Genre Packs)

출시 시기: 2023년 1월

개념: 스키니 번들(skinny bundle) 형태로, 불필요한 채널을 줄인 합리적 가격대의 상품

예시:

월 70달러 ‘MySports’

월 35달러 ‘MyEntertainment’

추가 확장: 유료 프리미엄 채널 및 테마별 추가 상품 확대

3) 시그니처(Signature) 패키지

특징: 90개 이상의 채널을 포함하는 전통적 풀 번들(pay TV)

요금: 월 85달러부터 시작

전송 방식: 위성 대신 스트리밍으로도 시청 가능

4) 디폴트 셋톱박스는 ‘DirecTV 앱’

변화 포인트: 별도 위성 셋톱박스 없이, OTT 서비스처럼 스마트 TV나 모바일 기기에 앱만 설치

장점: 장비 구매·설치 부담이 줄어들고, 가입 과정이 간편해짐

5) Gemini Air

특징: 안드로이드 TV 기반 동글(dongle) 기기

요금: 월 10달러 임대 가능

의의: 스트리밍 기기가 없는 고객을 위해 자체 개발 장치를 제공

1. Revamped Service Lineup

1) MyFree DirecTV (FAST Channel)

Launch Date: October 2022

Key Features: Provides 100 channels under a free, ad-supported streaming television (FAST) model

How to Watch: No subscription necessary; available free via the DirecTV app

2) Genre Packs

Launch Date: January 2023

Concept: Offers “skinny bundles,” eliminating unnecessary channels for a more cost-effective experience

Examples:

MySports at $70/month

MyEntertainment at $35/month

Expansion: Premium channels and themed bundles will continue to grow

3) Signature Package

Highlights: Over 90 channels in a traditional pay-TV bundle

Pricing: Starts at $85/month

Streaming Option: Available via satellite or streaming

4) ‘DirecTV App’ as the Default Set-Top

Change Point: Replacing dedicated satellite STBs with an OTT-like model where users install an app on smart TVs or mobile devices

Advantages: Eliminates set-top box purchasing/installation, simplifies the subscription process

5) Gemini Air

Characteristics: Android TV-powered streaming dongle

Monthly Fee: $10 rental option

Purpose: A proprietary device for customers who don’t own a streaming player

2. 배경: TPG 주도 하의 구조조정

디렉TV는 AT&T로부터 완전히 분리된 뒤, 사모펀드 TPG(Inc.) 주도 하에 대대적인 구조조정을 추진해 왔다.

광대역 인터넷 사용이 편리한 도시 지역에는 앱 기반 스트리밍 가입을 안내하고, 인터넷 환경이 열악한 농촌 지역에 한해서만 위성 TV를 유지하는 방식으로 서비스를 이원화했다.

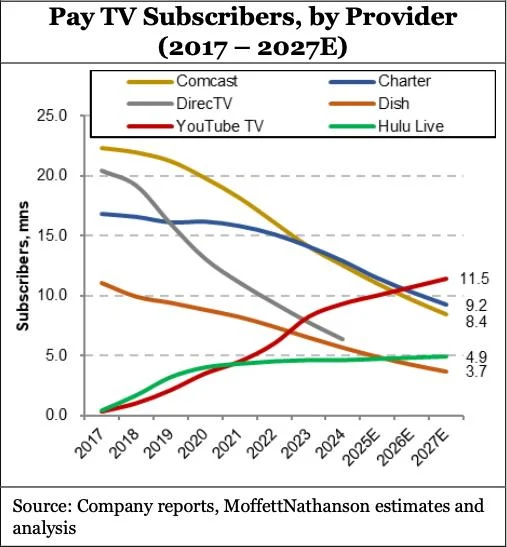

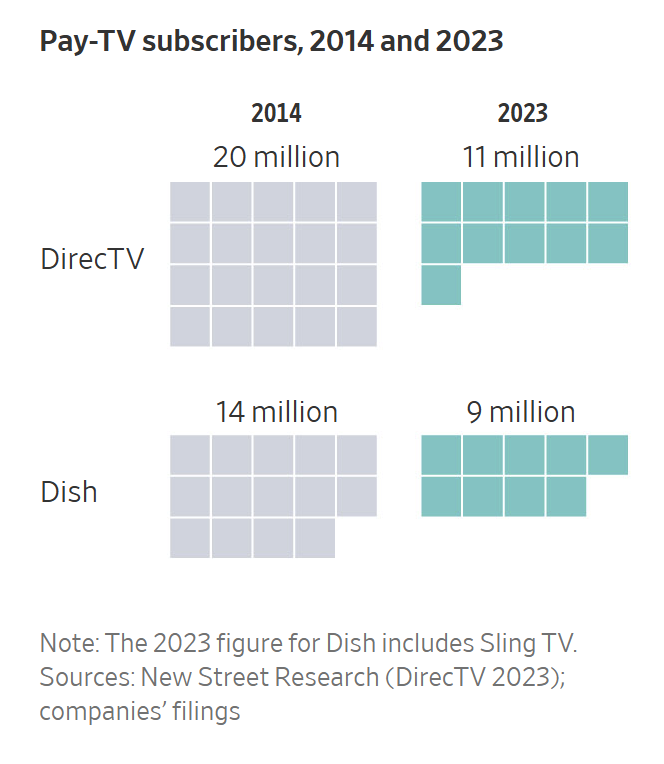

내부 관계자에 따르면, 2023년 9월 기준 위성·스트리밍·과거 U-verse를 모두 합쳐 약 1,100만 명의 가입자를 보유하고 있는 것으로 전해진다.

그러나 스트리밍 서비스로의 전환이 급속도로 진행되고 있어 위성방송의 구독자 감소는 계속될 전망이다.

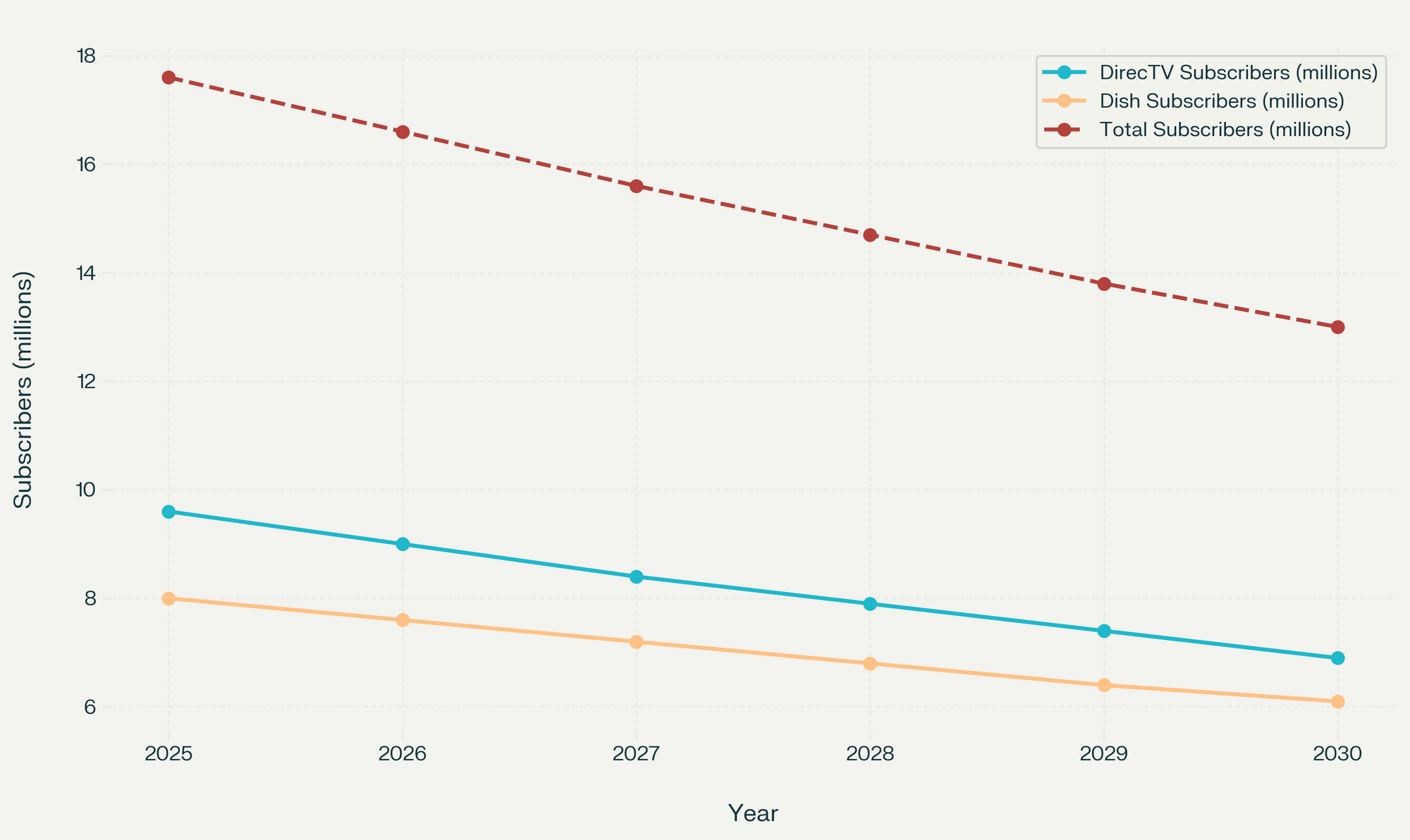

2025년~2030년 디렉TV 가입자 수 변화 분석 및 예측

현재 추세 분석:

- DirecTV: 2014년 2,000만 명에서 2023년 1,100만 명으로 45% 감소

- Dish(Sling TV 포함): 2014년 1,400만 명에서 2023년 900만 명으로 36% 감소

감소 추세는 스트리밍 서비스 성장으로 인해 앞으로도 계속될 것으로 예상. 연간 감소율을 기반으로 예측을 진맹

예상 가입자 수 (단위: 백만 명):

| 연도 | DirecTV | Dish (Sling 포함) | 총 위성방송 가입자 |

|---|---|---|---|

| 2025 | 9.6 | 8.0 | 17.6 |

| 2026 | 9.0 | 7.6 | 16.6 |

| 2027 | 8.4 | 7.2 | 15.6 |

| 2028 | 7.9 | 6.8 | 14.7 |

| 2029 | 7.4 | 6.4 | 13.8 |

| 2030 | 6.9 | 6.1 | 13.0 |

2. Background: TPG-Led Restructuring

After fully separating from AT&T, DirecTV began an extensive overhaul under private equity firm TPG. In urban areas with reliable broadband, it now steers customers toward app-based streaming, while retaining satellite TV primarily for rural and underserved regions. As of September 2023, DirecTV reportedly has around 11 million subscribers across its satellite, streaming, and legacy U-verse platforms.

3. 경쟁 환경 및 전략 변화

1) 반독점 소송과 장르별 요금제 도입

디렉TV는 지난해 스포츠 스트리밍 합작사 ‘Venu Sports’를 상대로 푸보(Fubo)와 함께 반독점 소송을 지원해, 디즈니·폭스·워너브라더스 디스커버리 등 대형 방송사의 채널 편성 권한 제한을 일부 해제하는 데 성공했다.

이를 통해 특정 장르에 한정된 채널 묶음(Genre Packs)을 합리적으로 구성할 수 있게 되었고, 고객 이탈과 비용 부담을 동시에 줄일 수 있는 토대를 마련했다.

2) 앱 기반 스트리밍 전환 가속

위성 방송은 유지 비용이 많이 들고, 가입자를 모으기가 점차 어려워지고 있다. 이에 비해 앱 기반 스트리밍 서비스는 인프라 부담이 적어, 디렉TV는 스트리밍 상품을 대폭 강화하고 있다. 무료 광고 기반 MyFree DirecTV부터 스키니 번들, 풀 번들까지 폭넓은 선택지를 마련해 다양한 소비자군을 공략 중이다.

4. 분석: 소비자 맞춤형 전략과 가입자 유입 효과

1) 스키니 번들 확대

과거 전체 채널을 망라했던 풀 번들을 부담스러워하던 이용자층을 위해, 스포츠나 엔터테인먼트 등 관심 장르에 맞춰 채널만 묶어 판매한다. 이는 가격 문턱을 낮추고 특정 취향에 최적화된 시청 경험을 제공한다.

2) 무료+유료 혼합 모델 구축

FAST(무료 광고 기반 스트리밍) 서비스인 MyFree DirecTV로 고객을 먼저 유입시키고, 이후 상위 유료 상품으로 전환시키는 구조가 마련됐다. 이는 넓은 사용자 풀을 확보하면서도 프리미엄 상품 판매를 통한 수익 창출을 기대할 수 있다.

3) 낮아진 기술·디바이스 장벽

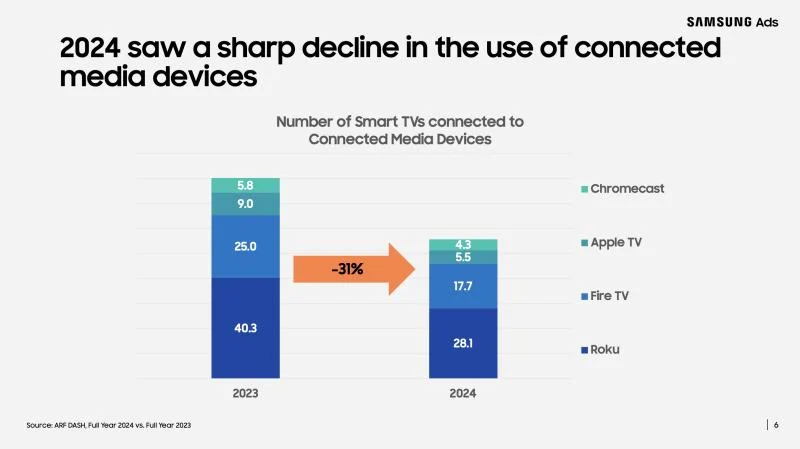

스마트 TV나 스트리밍 기기만 있으면 셋톱박스 없이 가입이 가능하다. Gemini Air 동글 역시 월 10달러 임대 방식으로 제공돼, 하드웨어 장벽을 최소화한다. 신규 가입자를 끌어들이는 데 유리한 요소다. 그러나 장기적으로 동글 역시 시장 전망이 녹녹치 않다. 스마트TV 등 커넥티드TV의 수요가 급격히 증가하고 있기 때문이다.

삼성애즈가 집계한 보고서(Q1 2025 State of Video report)에 따르면 2024년 미국에서 스마트 TV에 연결된 외부 스트리밍 기기의 수는 31% 감소했다. 2023년 미국 스마트 TV에 연결된 HDMI 동글, 하키 퍽 등기타 스트리밍 주변기기가 4,030만 개에서 2024년에는 2,810만 개에 불과한 것으로 나타났다.

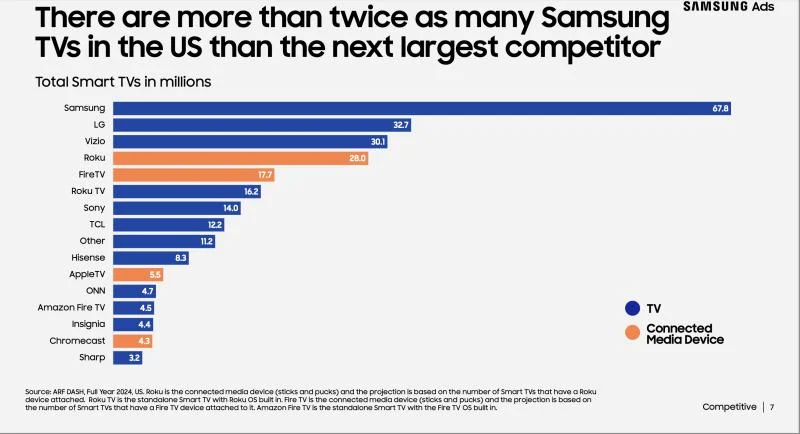

그러나 스마트TV 판매가 계속 증가하고 있다. Roku 등에서 내장 운영체제를 탑재한 스마트 TV는 계속 판매되고 있으며, 미국의 스마트 TV 보급률은 여전히 견고하다. 보고서에 따르면, 스마트 TV는 현재 미국 내 1억 2,200만 TV 가구의 83%, 전체 1억 3,300만 가구의 77%에 보급되어 있다.

삼성전자는 미국 가정에 설치된 스마트 TV가 6,780만 대로 시장을 선도하고 있으며, 이는 2위인 LG의 두 배가 넘는 수치다. 삼성 스마트 TV는 미국 전체 스마트 TV의 32%를 차지하고 있으며, 미국 스마트 TV 가구의 45%에 설치되어 있다.

3. Competitive Landscape and Strategic Shifts

1) Antitrust Victory and the Emergence of Genre Packs

Last year, DirecTV supported Fubo’s antitrust lawsuit against sports-streaming joint venture Venu Sports, forcing Disney, Fox, and Warner Bros. Discovery to loosen some channel-packaging restrictions. This allowed DirecTV to offer narrowly focused channel bundles (Genre Packs) that mitigate churn and reduce cost burdens.

2) Accelerated Move to Streaming

Satellite television is expensive to maintain and increasingly less attractive to new subscribers. By contrast, app-based streaming is less capital-intensive and more flexible. DirecTV is thus ramping up its streaming offerings, from free ad-supported channels (MyFree DirecTV) to skinny bundles and full-scale premium bundles.

4) 콘텐츠 협상력 강화

장르별 요금제 판매를 위해선 다양한 채널 공급사와 새로운 협상이 필요하다. 디렉TV는 반독점 소송으로 얻은 유연성을 바탕으로, 이런 협상에서 이점을 확보해 앞으로도 상품 경쟁력을 높일 것으로 전망된다.

4 디렉TV와 한국 방송 시장

장르팩과 FAST채널의 확산

국내에서도 ‘알아서 골라보는’ 채널에 대한 수요가 계속 제기되어 왔다. 디렉TV의 성공 여부가 IPTV·케이블TV 등 국내 유료방송 사업자가 향후 상품 전략을 짜는 데 실제 참고자료가 될 가능성이 높다.

아울러 FAST와 유료 방송 채널이 결합되는 '기술 중립' 이른바 하이브리드 번들은 한국에서도 자리 잡을 가능성이 크다. 일단 CJ ENM, KBS 등 국내 주요 사업자들도 무료 광고 기반 스트리밍 채널(FAST)을 선보였거나 검토 중이다. 디렉TV처럼 무료 채널로 유입을 늘리고, 일부를 유료 상품으로 흡수하는 모델이 국내 방송·OTT 업계에도 유효한 전략이 될 수 있다.

디렉TV가 앱을 기본 셋톱박스로 삼은 것처럼, 한국에서도 스마트 TV와 스트리밍를 병행하는 이용자가 갈수록 늘어나는 추세다.

콘텐츠 편성·협상 구조 변화

스트리밍 서비스의 확산, 유료 방송의 장르별 채널 묶음이 확산되면 방송 시장 거래 구조에도 변화를 수반할 수 밖에 없다. 특히, 동시에 한국에서도 방송사와 스트리밍·유료방송 플랫폼 간 권리 협상 구조가 달라질 수 있다. 채널 공급사(PP) 입장에서도 편성을 더 유연하게 열어둘 필요성이 높아질 것으로 예상된다. 동시에 재전송료, 프로그램 사용료 등에도 변화가 불가피하다. 시청자를 위한 채널 거래 정책이 필요하다.

농촌·도서지역 등 망 문제

한국은 광대역망 보급률이 세계적으로 높은 편이지만, 인터넷 환경이 제한적인 군부대·도서산간 지역이 존재한다. 디렉TV처럼 위성과 스트리밍 서비스를 병행하는 전략은 국내 일부 지역·특수기관에도 적용될 만한 사례로 평가된다. 아직은 유효하다.

4 Implications for the Korean Broadcasting Market

1) Skinny Bundle Lessons

Korean pay-TV operators have long contemplated “pick-and-choose” channel structures. DirecTV’s progress could inform local IPTV and cable providers on rolling out similar tiered or themed bundles.

2) Rising Trend of FAST Services

Major Korean broadcasters such as CJ ENM and KBS are experimenting with free ad-supported streaming (FAST). DirecTV’s model—using free channels to grow its audience before upgrading some to premium subscriptions—offers a compelling case study for Korean OTT and broadcasters.

3) Strengthening the Shift to Streaming

DirecTV’s move to make the app its default STB exemplifies the ongoing shift away from traditional hardware in favor of over-the-top solutions. In Korea, a large portion of IPTV and cable subscribers also use smart TVs or OTT platforms, suggesting local broadcasters may similarly accelerate their OTT strategies.

4) Evolving Content Distribution and Rights Negotiations

As targeted channel packs take hold, content providers may need to be more flexible about how their channels are packaged and sold. This potential shift could also reshape contracts between Korean broadcasters and local OTT or pay-TV operators.

5) Addressing Rural and Remote Areas

While Korea’s broadband coverage is extensive, some remote or military areas face connectivity challenges. DirecTV’s dual approach—streaming for connected regions and satellite for underserved areas—could inspire Korean operators to consider hybrid solutions combining DMB, LTE, or satellite brodcasts with Streaming

결론

디렉TV는 위성 방송의 상징적인 지위를 내려놓고, 스트리밍 시대에 발맞춘 ‘앱 기반’ 서비스로 빠르게 전환하고 있다. 약 1,100만 명의 가입자를 기반으로, 무료 FAST부터 장르별 스키니 번들, 풀 번들까지 폭넓은 상품을 선보이며 다양한 고객층을 공략한다. 이는 사모펀드 TPG 주도 하에 진행되는 구조조정과, OTT 스트리밍이 주류가 된 미국 시장 상황에 대응하기 위한 선택으로 풀이된다.

디렉TV의 이 같은 움직임은 한국 방송·스트리밍 시장에도 시사점을 준다. 스키니 번들, FAST 서비스, 앱 중심 시청 환경, 콘텐츠 편성 유연화 등은 이미 국내에서도 주목받고 있는 화두다. 앞으로 한국에서도 장르별 채널 판매나 무료 광고 기반 채널 확대, 그리고 OTT 우선 전략이 얼마나 빠르게 안착할지에 따라 유료방송과 OTT 업계의 경쟁 구도가 크게 달라질 전망이다

Conclusion

DirecTV is leaving its “satellite TV” legacy behind, reorienting toward an app-based streaming model to meet the needs of modern viewers. Its estimated 11 million subscribers can choose from free ad-supported channels, targeted genre packs, or comprehensive premium bundles, all under the TPG-led restructuring that aims to control costs and tap new subscriber segments.

This transformation resonates in the broader landscape, including Korea, where cable, IPTV, and OTT providers are observing similar shifts. Skinny bundles, FAST services, flexible channel packaging, and an app-first strategy are among the concepts poised to shape the next phase of the Korean media market. As operators embrace new bundling and distribution models, the ultimate question is how quickly consumers will adapt—and whether these offerings will meaningfully reduce churn while attracting new viewers.